Table of Contents >> Show >> Hide

- What Generational Wealth Inequality Actually Means

- Why the Gap Keeps Growing

- The Nuance: Younger Adults Are Not Uniformly Doomed

- How Generational Wealth Inequality Shows Up in Real Life

- Why This Matters Beyond Individual Households

- What Could Help Narrow the Gap

- Conclusion

- Experiences Related to Generational Wealth Inequality

- SEO Tags

Money is supposed to be a tool. In real life, it often behaves more like a relay baton. One generation grabs it, runs as far as possible, and then hands it off to the next. The families that start the race with a house, a retirement account, and maybe a grandparent who thinks “trust fund” is a love language usually keep moving. Families starting with debt, unstable housing, and a financial cushion thinner than a paper napkin? They spend more time catching their breath than building wealth.

That is the heart of generational wealth inequality. It is not just about who earns more this year. It is about who owns assets, who benefits from time and compounding, who gets help with a down payment, who inherits property, and who begins adult life already carrying financial weight. Income pays the bills. Wealth changes the storyline.

In the United States, the wealth gap is not just big. It is sticky. It can survive recessions, inflation, housing booms, college tuition spikes, and every cheerful speech about “personal responsibility” ever delivered from a podium. And because wealth moves through families, what happened to your parents and grandparents often matters almost as much as what happens on your own paycheck.

What Generational Wealth Inequality Actually Means

Generational wealth inequality describes the uneven way assets and financial security are distributed across age groups and passed from one generation to the next. It includes differences between younger adults and older adults, but it also includes differences within generations. Two people can both be millennials and still be living on entirely different economic planets if one received family help with college and housing while the other started adulthood with student loans and no safety net.

Wealth is usually measured as net worth: everything a household owns minus everything it owes. That includes home equity, retirement savings, checking and savings accounts, stocks, business ownership, and other assets, minus debts like mortgages, student loans, credit cards, and auto loans.

Here is the key distinction: income is a stream, but wealth is a reservoir. A family with decent income but no assets can still be one emergency away from trouble. A family with assets can absorb shocks, invest in opportunities, move to a better school district, help a child with college, or support a first home purchase. Wealth buys time, flexibility, and fewer panic attacks at 2 a.m.

Why the Gap Keeps Growing

1. Asset ownership does the heavy lifting

The biggest drivers of household wealth in America are not mysterious. They are usually a home and retirement savings. That means families who buy homes earlier and contribute to retirement accounts sooner tend to build wealth faster. Families who rent longer, delay saving, or never gain access to appreciating assets often fall behind even when they work just as hard.

This is where generational wealth inequality gets sneaky. Once a family owns appreciating assets, those assets often do more work than the family does. Home values rise. Investments compound. Tax advantages kick in. Meanwhile, families without those assets spend more of their income on rent, interest, and recovery from setbacks. The result is a classic rich-get-richer dynamic, except dressed in khakis and holding a mortgage statement.

2. Housing is still the main wealth machine

For most middle-class families, homeownership remains the primary way wealth is built and transferred. But buying a home has become harder for younger households. High prices, larger down payments, tougher borrowing conditions, and elevated mortgage rates have made the path to ownership look less like a staircase and more like a rock wall.

That matters because owning a home does more than provide shelter. It builds equity, creates a stable payment base if a fixed mortgage is involved, and becomes something that can eventually be borrowed against, sold, or passed down. Renters do not get none of these benefits. They get a front-row seat to annual lease increases and a very intimate relationship with move-in fees.

When younger adults enter the housing market late, they lose years of appreciation and equity growth. When they never enter at all, the wealth gap can become permanent. A generation can be highly educated, technologically fluent, and capable of building a six-tab budget spreadsheet while still struggling to buy the kind of starter home their parents once considered glorified plywood.

3. Debt delays the launch

Debt is not always bad. A mortgage can help build wealth. Business credit can support growth. But some debt acts more like a speed bump placed every ten feet. Student loans are one example. Education can raise earnings over time, but the debt tied to it can delay wealth-building milestones in the short run, especially homeownership and emergency savings.

That tradeoff matters because early adulthood is when financial trajectories begin to harden. If a person spends their twenties and early thirties paying down debt, renting, and postponing retirement contributions, they miss years of compounding. Wealth-building is heavily influenced by timing, and lost time is expensive. Compounding is kind to the early saver and absolutely ruthless to the late starter.

4. Inheritance is not everything, but it is definitely something

Not every family passes down a mansion, a brokerage account, or a vacation cottage with a dock and too many opinions. But even modest transfers matter. A used car. Help with tuition. A place to live after graduation. Assistance with a security deposit. Money for a down payment. A fully paid funeral bill so a crisis does not become a financial crater. These forms of family support do not always show up in splashy headlines, but they shape life chances in profound ways.

Inheritance and inter vivos transfers, or gifts given while someone is still alive, help explain why wealth inequality can persist across generations. Families with wealth often help younger relatives avoid debt, invest earlier, and recover faster from setbacks. Families without wealth may provide emotional support, childcare, and housing when possible, but they often cannot provide the same financial lift. Love may be free. Down payments are not.

5. Recessions do not hit everyone equally

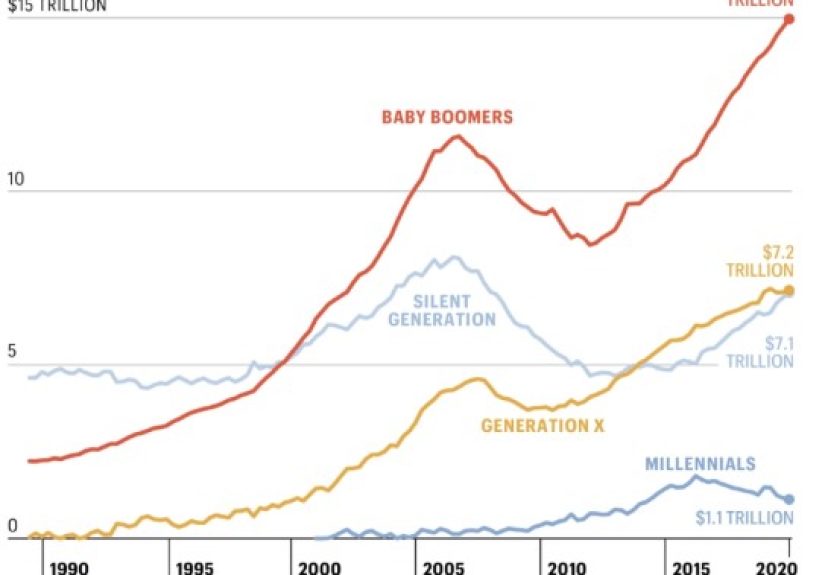

Generations are shaped by the economy they meet at adulthood. People entering the labor market during a recession often face lower wages, fewer job options, and slower wealth accumulation for years. Millennials, for example, were deeply affected by the Great Recession and the housing collapse. Many started their careers during a weak job market and delayed homebuying, marriage, and family formation.

When wages begin lower and asset ownership starts later, catching up becomes difficult. Even if incomes improve later, the lost years of compounding and appreciation can leave a lasting scar. That is why generational wealth inequality is not simply about personal habits. Timing matters. So do the macroeconomic events people cannot control.

The Nuance: Younger Adults Are Not Uniformly Doomed

A smart discussion of generational wealth inequality needs one important correction: the story is not pure collapse. Recent data suggest that younger households have made stronger gains than many people expected, especially after pandemic-era changes in savings, asset values, and labor markets. Some younger adults built wealth faster than earlier research predicted.

Still, that does not erase the larger structural problem. Even when younger households improve their position at the same age compared with prior generations, they usually still control a smaller share of total national wealth than older households. They also remain more vulnerable to housing costs, debt burdens, and uneven access to family support.

So yes, some younger families are doing better than the bleakest headlines suggest. But a few encouraging charts do not mean the game is fair. It means the scoreboard is complicated.

How Generational Wealth Inequality Shows Up in Real Life

Family A buys time; Family B buys survival

Imagine two households with similar annual incomes. One received help with college, got a small inheritance, and used family money for a home down payment. The other graduated with debt, rented through multiple rent hikes, and sent money back home during a parent’s medical crisis. On paper, they may look like neighbors. In reality, one family is compounding wealth while the other is absorbing shocks.

The difference shows up everywhere. One household can put money into retirement and a 529 plan. The other focuses on minimum payments and avoiding overdraft fees. One can take career risks, relocate, or start a business. The other needs stability at all costs. One builds equity. The other builds resilience, which is admirable but does not appear in net worth calculations.

Older wealth can shelter younger adults

When parents or grandparents own homes outright, have retirement savings, and can provide informal support, younger family members often avoid the most damaging financial mistakes. They can move back home without paying market rent. They may receive childcare support that keeps them in the workforce. They can borrow from family instead of turning to high-interest credit.

That does not make those families lazy or spoiled. It makes them connected to an existing asset base. Meanwhile, families without those resources must solve every problem at retail price. And retail price, as the modern economy loves to remind us, is rude.

Why This Matters Beyond Individual Households

Generational wealth inequality is not just a private family matter. It has broad consequences for economic mobility, consumer demand, neighborhood stability, and even democratic trust. When large groups of younger adults feel locked out of homeownership, secure retirement planning, and basic asset-building, the economy becomes more fragile.

Low wealth also affects health, education, and entrepreneurship. Families with assets can handle a medical bill, help a child through a rough semester, or survive a business slow period. Families without assets often have to cut back at the worst possible time. That leads to stress, reduced mobility, and fewer opportunities passed to the next generation.

In other words, wealth inequality today is opportunity inequality tomorrow.

What Could Help Narrow the Gap

Expand access to first assets

Policies that help people build initial assets matter a lot. That includes first-time homebuyer support, down payment assistance, emergency savings incentives, and easier access to retirement plans through automatic enrollment. The first chunk of wealth is usually the hardest to build. After that, momentum helps.

Reduce the penalties of starting adult life in debt

Making higher education more affordable, simplifying repayment options, and protecting borrowers from spiraling delinquency can reduce the drag debt places on early wealth-building. This is not about pretending debt disappears by positive thinking. It is about making sure education functions as a ladder instead of a cinder block tied to the ankle.

Make housing less exclusionary

More housing supply, zoning reform, starter-home construction, legal support for heirs’ property, and fair access to credit can all improve the odds that younger and lower-wealth households actually get a chance to own. A wealth-building system centered on housing cannot work well if housing remains inaccessible to huge portions of the population.

Support intergenerational transfers for families without wealth

That can mean estate planning help, matched savings accounts, baby bonds proposals, stronger tax credits for low- and middle-income households, and policies that make saving possible without losing public benefits. Wealth-building should not be reserved for families that already own plenty of it.

Conclusion

Generational wealth inequality is really the story of how the past keeps showing up in the present wearing a nametag that says “financial reality.” It is about who gets a head start, who gets a backup plan, and who is expected to build from zero while carrying debt, rising rent, and an economy that keeps changing the rules.

The issue is not whether younger adults work hard enough. Most do. The issue is whether work alone can overcome unequal access to assets, inheritance, housing, and time. Often, it cannot. Wealth is cumulative, and inequality compounds just as efficiently as savings do.

The good news is that this problem is not mysterious. We know many of the forces behind it: asset ownership, housing access, family transfers, educational debt, and policy design. That means the gap is not inevitable. But closing it will require more than inspirational speeches and budgeting apps. It will require making wealth-building possible for people who were not born near it.

Experiences Related to Generational Wealth Inequality

One of the clearest ways to understand generational wealth inequality is to listen to the kinds of experiences families describe when they talk honestly about money. Not performative money. Not social media money. Real money, where a broken transmission or a rent increase can wreck the month.

Consider the experience of a young professional who has a decent salary, a graduate degree, and what looks like a stable life from the outside. She pays her bills on time, contributes something to retirement when she can, and does all the things personal finance articles tell her to do. But she also sends money to help her parents, carries student loan debt, and rents in a market where housing costs eat up a huge part of her income. Her friend from college earns about the same amount, yet bought a condo at 29 because his parents covered part of the down payment. Ten years later, one has equity and leverage; the other has excellent budgeting skills and a landlord who just raised the rent again. Same effort. Very different launchpads.

Another common experience comes from families who inherit responsibility instead of assets. A middle-aged son may become the financial coordinator for aging parents who have little savings and rising medical expenses. He is not receiving wealth from the older generation; he is transferring his own time and money upward to keep the family stable. That changes what he can save for his own children. It changes whether he can invest, whether he can move, even whether he can take a better job in another city. In this version of family economics, love flows freely, but wealth flows in reverse.

There is also the experience of the family home as both blessing and battleground. For some households, a paid-off home becomes the one major asset that can be passed on. That house may help adult children avoid displacement, borrow against equity, or finally get a little breathing room. But when there is no will, unclear title, or unresolved heirs’ property issue, the home can become legally tangled and financially fragile. Instead of becoming a stable bridge between generations, it becomes a source of stress, fees, and conflict. The asset exists, but the transfer system fails.

And then there is the quiet experience many people do not talk about enough: the emotional effect of always feeling one step behind. People living with generational wealth inequality often describe a constant sense of delayed adulthood. They postpone children, homeownership, career changes, and even routine healthcare because the margin for error is too small. Their peers may look only slightly ahead, but the gap feels enormous because it is not just about money. It is about confidence, flexibility, and the ability to imagine a future that is not permanently defensive.

These experiences matter because they remind us that wealth inequality is not just a chart problem. It shapes daily choices, family relationships, and long-term hope. It tells some people that the future is something to build, while telling others the future is something to survive. That difference is exactly why generational wealth inequality deserves serious attention.