Table of Contents >> Show >> Hide

- Why People Think the Market Predicts the Future

- What the Stock Market Actually Predicts Pretty Well

- Where the Stock Market Fails Miserably

- Real Examples: When the Market Looked Smart and When It Looked Silly

- So, Can the Stock Market Predict the Future?

- How Smart Investors Should Use Market Signals

- Experiences Related to “Can the Stock Market Predict the Future?”

- Conclusion

If the stock market had a superpower, it would not be mind reading. It would be rumor collecting at lightning speed, overreacting before lunch, calming down by dinner, and then pretending it was rational the whole time.

That is exactly why people keep asking whether the stock market can predict the future. Stocks move before headlines become obvious. Markets often wobble before recessions are officially declared. Sectors tied to technology, housing, banks, or consumer spending can start whispering about tomorrow long before economists finish polishing their forecasts. So yes, the market can seem spooky-smart.

But here is the catch: the market does not predict the future. It prices possible futures. That is a huge difference. It is less crystal ball, more probability machine wearing expensive shoes.

The best answer is this: the stock market can offer useful clues about where the economy, earnings, interest rates, and investor sentiment may be headed, but it is not a flawless oracle. Sometimes it spots trouble early. Sometimes it screams “fire” in a crowded theater and then remembers it was just burnt toast.

Why People Think the Market Predicts the Future

Stock prices are forward-looking by design. When investors buy or sell shares, they are not paying for yesterday’s revenue or last quarter’s drama. They are trying to estimate future profits, future borrowing costs, future consumer demand, future policy moves, and future risk. In plain English, they are constantly asking, “What happens next?”

That is why the market often moves months before the real economy shows the same trend. By the time a recession is confirmed, stocks may already have fallen and started recovering. By the time a recovery feels obvious to regular people, the market may already be pricing in the next slowdown. Annoying? Yes. Fascinating? Also yes.

Stocks Discount Expectations

The market is basically a giant discounting machine. Investors estimate what future cash flows might look like, then adjust those expectations for risk, interest rates, inflation, competition, and a thousand other variables. If future earnings seem stronger, stock prices can rise before the earnings actually arrive. If rates look set to stay high, stock valuations can cool before the damage fully shows up in business results.

This is why market rallies can happen when current news still looks ugly. It is not always because investors are irrational. Sometimes the market is simply looking six to twelve months ahead while everyone else is still arguing about last month.

The Market Reacts Faster Than Most People

Millions of investors, analysts, hedge funds, pension managers, algorithms, and institutions are constantly processing new information. Economic data, company guidance, bond yields, oil prices, geopolitical shocks, Fed language, and consumer trends all get absorbed into prices at breathtaking speed.

In theory, that makes the market a useful forecasting tool. In practice, it also makes the market noisy, emotional, and occasionally dramatic enough to deserve its own reality show.

What the Stock Market Actually Predicts Pretty Well

The market is not equally good at predicting everything. It tends to do better with broad direction than with exact timing, and better over longer horizons than over the next few days.

1. It Can Signal Changes in Economic Direction

A falling stock market can hint that investors expect slower growth, weaker profits, tighter credit, or rising stress ahead. That does not mean every sell-off leads to recession. Still, markets often weaken before the economy does because investors are adjusting to future conditions, not current comfort.

More specifically, markets tied to expectations can be valuable. Bank stocks may react to credit stress. Consumer discretionary names can soften when households look stretched. Cyclical industries such as manufacturing, semiconductors, transports, and housing-related companies can sometimes provide early signals about business conditions.

That said, many economists would argue that the bond market, especially the yield curve, has historically been a cleaner recession signal than the stock market alone. Stocks can hint. Yields often speak more clearly.

2. It Can Offer Useful Clues About Long-Term Returns

If you are asking whether the market can predict what happens next week, the answer is mostly no. If you are asking whether valuations can shape likely returns over the next decade, the answer gets much more interesting.

Metrics such as the Shiller CAPE ratio, price-to-earnings multiples, and market-cap-to-GDP are imperfect but useful. When valuations get extremely stretched, future long-term returns often become more muted. When markets are deeply cheap after panic-driven sell-offs, long-run expected returns usually improve.

This does not mean high valuations tell you the exact day a bull market ends. Markets can stay expensive longer than logic would prefer. But valuation does help frame what kind of decade investors may be buying into. In other words, it is not a clock. It is more like a weather pattern.

3. It Can Reflect Short-Term Fear Through Volatility

Measures like the VIX are often called the market’s fear gauge. They do not tell you whether the world ends on Tuesday, but they do capture how much turbulence investors expect in the near term. That is useful because sentiment matters. When fear spikes, liquidity dries up, headlines get louder, and markets can swing harder than a caffeinated squirrel.

Volatility signals can help explain how uneasy investors are about the immediate future. They are less helpful if you want neat predictions about growth three years from now.

Where the Stock Market Fails Miserably

Here is where the mythology needs a haircut.

1. The Market Throws False Alarms

The famous joke is that the stock market has predicted nine of the last five recessions. The line has survived for a reason: stocks can overreact. Sharp declines do not always lead to economic collapse. The 1987 crash was brutal, but it did not produce a full-blown recession. Markets can panic, then recover, leaving everyone emotionally exhausted and financially confused.

This is one reason investors get into trouble when they treat every correction like a prophecy. A market sell-off may be a warning. It may also be a tantrum.

2. The Stock Market Is Not the Economy

This point cannot be overstated. The stock market is a collection of publicly traded companies, not a complete portrait of every worker, every household, every small business, or every town in America.

Large-cap indexes are heavily influenced by major corporations, many of which earn revenue around the world. That means stock prices can rise even while parts of the domestic economy feel weak. It also means a handful of giant companies can make the market look healthier than the average family budget.

That disconnect became especially obvious in the pandemic era. The market rebounded quickly while many households, workers, and small businesses were still navigating a real-world mess. Market prices were reacting to stimulus, rates, expected earnings, and future recovery. Human beings were reacting to reality, which tends to be less elegant.

3. Short-Term Price Moves Are Often Unpredictable

Even strong believers in market efficiency make this point: if prices already reflect available information, then short-term moves should be very hard to predict consistently. That is why beating the market repeatedly is so difficult.

On any given day, stocks can move because of earnings guidance, macro data, options flows, positioning, geopolitics, rate expectations, or the simple fact that markets are full of humans who occasionally lose their minds in groups.

The closer your time horizon gets to “this afternoon,” the more the market behaves like a weather vane in a wind tunnel.

Real Examples: When the Market Looked Smart and When It Looked Silly

The Dot-Com Bubble

In the late 1990s, investors priced technology as if the future had arrived early and would only get shinier. In one sense, they were right: the internet did transform the economy. In another sense, they were wildly early and wildly overpriced. The market correctly sensed a massive technological shift, but it got carried away on valuation. That is a classic example of the market predicting a real trend while badly mispricing the timeline and scale.

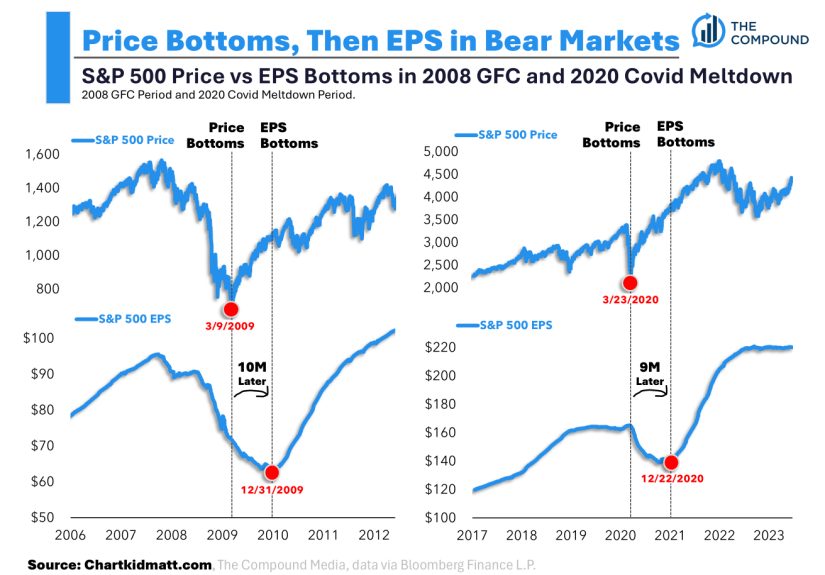

The 2008 Financial Crisis

Stocks began falling well before the full damage of the crisis was obvious to the public. Credit markets, bank shares, housing-related businesses, and financial stress indicators signaled deep trouble. In that case, markets were not just being moody. They were picking up real deterioration.

But even there, the market was not cleanly prophetic. Some investors saw the danger early. Many did not. Panic intensified once the crisis was underway. The market gave clues, but not a tidy memo labeled “Here is exactly what happens next.”

The 2020 Pandemic Shock and Recovery

The COVID recession officially lasted from February to April 2020, an extraordinarily brief but severe contraction. The market collapsed fast and then rebounded fast, long before life felt normal. That rebound looked absurd to many people at the time. Yet markets were pricing stimulus, low rates, reopening potential, and the earnings power of large companies that could survive or even benefit from the shift.

Was the market right? In some ways, yes. Was it detached from everyday economic pain? Also yes. This is the perfect reminder that markets can anticipate recovery while society is still living through the storm.

So, Can the Stock Market Predict the Future?

Yes, but only in the way probabilities predict the future.

The stock market can:

- signal changing expectations about growth, inflation, profits, and rates,

- provide rough guidance about long-term return potential through valuation,

- reflect investor fear or optimism in real time, and

- sometimes move ahead of the broader economy.

The stock market cannot:

- consistently forecast exact turning points,

- tell you whether a correction becomes a recession,

- predict short-term prices with reliable precision, or

- serve as a complete stand-in for the real economy.

The market is best understood as a giant voting machine for expectations, with prices adjusting constantly as new information arrives. Sometimes that process is brilliant. Sometimes it is embarrassingly dramatic. Most of the time, it is both.

How Smart Investors Should Use Market Signals

Instead of asking the market for prophecy, it is smarter to ask it for context.

Use the Market as One Indicator, Not the Only Indicator

Smart analysis combines stocks with bond yields, credit spreads, labor data, inflation trends, earnings revisions, consumer spending, and business sentiment. The market can be an early clue, but the full picture requires more than one dashboard light.

Respect Valuation, but Do Not Worship It

High valuations can suggest lower long-term returns. Low valuations can suggest better future opportunity. But valuation rarely works as a perfect timing device. Expensive markets can get more expensive. Cheap markets can stay unloved for longer than your patience would prefer.

Avoid Turning Every Headline into a Trading Signal

Markets move fast. Narratives move faster. If you chase every scary headline or euphoric rally, you may end up buying high, selling low, and developing a deeply personal relationship with regret.

Long-term investing works better when you understand what the market is good at signaling, while accepting what it will never deliver: certainty.

Experiences Related to “Can the Stock Market Predict the Future?”

One of the most common investor experiences is the strange feeling that the market knows something before everyone else does. A person wakes up, sees stocks down sharply for three straight weeks, and starts wondering whether layoffs, recession, or some other disaster is around the corner. That instinct is understandable. Markets often move before the economy shows visible cracks. But the experience can be misleading because the market is not reacting to one future. It is reacting to many possible futures at once.

Another common experience happens during rallies. Economic news still feels shaky, inflation is annoying, people are grumbling about grocery bills, and yet stock indexes keep climbing. To many ordinary observers, that feels ridiculous. But the market may be looking past today’s discomfort and pricing better earnings, lower future rates, or improving productivity six to twelve months out. This creates a frustrating emotional gap: people experience the present, while markets keep trying to price the future.

Retirement investors often experience this question in the most personal way. When their 401(k) falls, it feels like a direct message from the universe that something bad is coming. Sometimes that fear is justified. Other times it is just volatility doing what volatility does. Many long-term investors eventually learn a tough lesson: the market can be early, wrong, or both. Selling every time prices drop may feel protective in the moment, but it can also lock in losses and miss recoveries that arrive before confidence returns.

Business owners and executives experience market forecasting differently. They may watch their company’s stock, industry peers, or sector ETFs for clues about customer demand, credit conditions, and hiring plans. A weakening market can make leaders more cautious, even before hard data softens. In this way, market signals can shape behavior and become part of the future they seem to predict. That feedback loop is part of what makes financial markets powerful. They do not just reflect expectations. They can influence decisions that affect the economy itself.

Younger investors often go through a different version of the same story. They enter the market during a hot streak, assume charts only go up, then meet their first correction and suddenly become amateur philosophers. They start asking whether markets are rational, manipulated, efficient, broken, or haunted. The experience is valuable. It teaches that prices do not move in straight lines, headlines do not equal truth, and confidence is easiest to maintain right before it is tested.

Over time, experienced investors usually develop a calmer relationship with the question. They stop asking whether the stock market can predict the future with magical accuracy. Instead, they ask what kind of future the market might be pricing right now, what assumptions are embedded in valuations, and what risks are being ignored. That shift matters. It turns the market from an oracle into a tool.

In the end, the lived experience of investing is less about discovering perfect predictions and more about learning to live with uncertainty. The market offers signals, probabilities, warnings, and opportunities. It does not hand out guarantees. Once investors accept that, they usually make better decisions, sleep better at night, and spend a lot less time treating every red day like a prophecy from Mount Doom.

Conclusion

So, can the stock market predict the future? Sort of. It can forecast expectations, probabilities, and long-run tendencies better than it can forecast exact events, dates, or daily moves. It can hint at recessions, reflect changing risk, and suggest whether future returns may be rich or restrained. But it can also panic, exaggerate, and send false alarms with the confidence of a man who gives directions while completely lost.

The smartest way to read the market is with humility. Listen to it. Learn from it. Compare it with other indicators. But do not confuse a fast-moving pricing machine with a fortune teller. The market may see ahead, but it rarely sees clearly.