Table of Contents >> Show >> Hide

- Why AI Valuations Keep Going Vertical

- Valuation Is Not Ownership

- OpenAI: The Most Public Example of a Very Private-Market Problem

- Why the Broader Market Makes This Even Trickier

- What Founders, Employees, and Early Investors Should Watch

- What This Feels Like on the Ground: of Real-World AI Deal Experience

- Conclusion

- SEO Tags

In the current AI boom, private-company valuations are behaving like they found an espresso machine and never looked back. Frontier labs, infrastructure plays, and enterprise AI startups are raising money at numbers that would have sounded like satire a few years ago. And yet, behind the champagne headline“Company X raises billions at a jaw-dropping valuation”there is often a less glamorous subplot: dilution.

That is the part many people skip because “$300 billion valuation” is a lot more exciting than “let’s discuss cap table mechanics.” But if you are a founder, early employee, angel investor, or anyone else who enjoys owning part of something valuable, the dilution story matters just as much as the valuation story. Sometimes more.

The simple version is this: a huge valuation does not guarantee a founder-friendly deal. In fact, in AI, the opposite can be true. Companies are so capital-hungrythanks to chips, cloud costs, research talent, safety work, data infrastructure, and now global compute buildoutsthat even enormous headline prices can come with meaningful ownership give-ups, option-pool resets, governance tradeoffs, and recapitalizations that change who really benefits.

OpenAI is the cleanest public example. It is not a perfect template for every startup, because OpenAI is not a normal company and has said so itself. But that is exactly why it is useful. If the market’s biggest AI darling still has to wrestle with structure, control, stock economics, and investor alignment, then smaller AI companies should assume those issues are not side quests. They are the main plot.

Why AI Valuations Keep Going Vertical

First, let’s give the valuation boom its due. Investors are not throwing darts at a whiteboard labeled “robot magic.” They are responding to a sector that combines blistering revenue potential with strategic urgency. AI is now viewed as foundational technology, not a cute software feature tucked behind a settings icon.

The best AI companies have several things investors love: large addressable markets, fast product iteration, sticky enterprise demand, and the possibility of platform dominance. If a model company becomes the default layer for coding, search, enterprise workflows, voice, agents, or national AI infrastructure, the upside is enormous. That possibility alone can justify aggressive pricing.

But AI is not just a software story. It is also an infrastructure story. The best labs need compute, and compute is expensive enough to make a normal SaaS CFO lie down in a dark room. This is why AI financings often balloon into mega-rounds. Capital is not merely fueling growth; it is buying time, talent, GPUs, data-center access, and strategic positioning.

That creates a weird market dynamic. The valuation gets bigger because the opportunity is bigger. But the capital raise also gets bigger because the company’s appetite for money is enormous. So even if the percentage sold in a single round looks manageable, the cumulative effect can still be severe over time. In other words, a larger pie is great. Selling many slices is less adorable.

Valuation Is Not Ownership

One of the most persistent startup myths is that a high valuation automatically protects everyone from dilution. It does not. It only tells you the price attached to the next financing. It does not tell you how many shares are being issued, what class of stock is being sold, what protective rights come with it, whether the option pool is expanding, or whether future restructuring will change the economics.

1. New-money dilution is still dilution

Start with the obvious part. If a company raises fresh money by issuing new shares, existing holders own a smaller percentage afterward. On basic post-money math, if a company raises $40 billion at a $300 billion post-money valuation, the new investors end up with roughly 13.3% of the company. The prior holders collectively go from 100% to about 86.7%.

That may not sound catastrophic. But repeat that processespecially in a capital-intensive category like AIand even elite companies can watch early ownership compress faster than expected.

2. Option-pool reloads quietly spread the pain

AI companies are in a ferocious talent war. They do not just need software engineers. They need model researchers, systems people, inference wizards, safety specialists, product leaders, chip whisperers, and the rare human who can explain transformer economics without causing a migraine.

That usually means generous equity grants and frequent refresh packages. If the company expands the employee option pool before or alongside a financing, the dilution often falls on existing common holders first. Founders may celebrate a flashy round, then discover the cap table has been “helpfully adjusted” in a way that feels like being thanked with an invoice.

3. Preferred terms can create economic dilution beyond the percentage math

Dilution is not only about how much of the company you own. It is also about how much your shares are worth in different outcomes. Preferred stock can come with liquidation preferences, anti-dilution protections, participation rights, and other terms that matter a lot when a company exits below the fantasy number everyone pitched in the deck.

In a booming market, people like to assume every winner will float upward forever. Real life is messier. If the company raises at an aggressive valuation and later grows into it more slowly than investors hoped, those protective terms can shift downside risk toward founders, employees, and common stockholders.

4. Secondaries are differentand that distinction matters

Not every eye-popping transaction is dilutive. A secondary sale, where existing shareholders sell shares to new buyers, usually does not create new shares. It changes who owns the pie, not how big the pie is.

But secondaries still matter because they reset price expectations, affect employee morale, create private-market benchmarks, and influence the next financing. In the AI market, tender offers and employee liquidity events have become increasingly important because many companies are staying private longer while valuations soar.

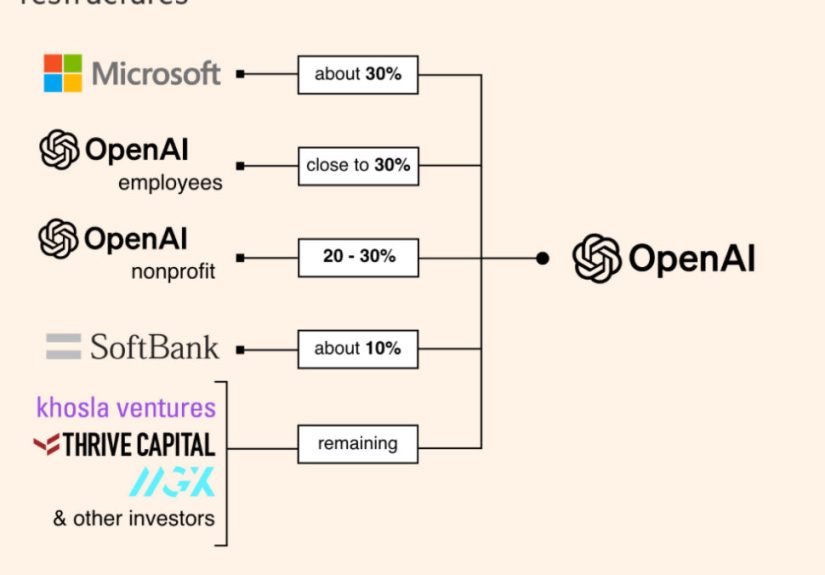

OpenAI: The Most Public Example of a Very Private-Market Problem

OpenAI is a particularly revealing case because the company’s structure has never been a boring vanilla cap table. In 2019, it introduced a capped-profit model: investors and employees could receive returns, but the nonprofit mission remained central, and the original nonprofit controlled the entity. That structure was designed to balance capital needs with mission constraints.

Then came the scale problem. As AI moved from research fascination to global platform race, OpenAI’s capital needs exploded. The company later announced one of the largest private financings in history: a round of up to $40 billion at a $300 billion valuation. That headline was astonishing, but so was the subtext. The money was tied to infrastructure, research expansion, and the broader need to finance industrial-scale AI development.

Here is where dilution and structure start doing a tango. A giant round at a giant valuation sounds gentle because the percentage sold may look smaller than in an early-stage round. But OpenAI’s public story showed that capital access was deeply linked to legal form, investor expectations, and governance. At one point, the funding was publicly described as contingent on a restructuring path. Later, OpenAI said the nonprofit would remain in control while the for-profit LLC would transition toward a Public Benefit Corporation structure.

Translation into plain English: this was not just a money-in, shares-out event. It was a larger negotiation about who controls the company, how future stock would work, how the mission would be preserved, and how investors could participate in upside.

OpenAI later said it was moving away from the more complex capped-profit design toward a more normal capital structure where everyone has stock, while the nonprofit would still control the enterprise and be a large shareholder. That is a huge clue for the rest of the market. When an AI company becomes large enough, the capital structure itself may have to evolve just to absorb the scale of financing required.

And that is where “massive valuation” can coexist with “massive dilution,” even if not always in the cartoonishly simple way people imagine. The dilution may happen in stages. It may be legal-structure dilution, economic-priority dilution, or future-stock dilution. It may show up in how new shares are issued, how old claims are converted, or how governance rights are redistributed.

OpenAI also highlights another important point: growth does not eliminate capital hunger. Even with surging revenue, top AI companies can still be staring at extraordinary compute spending. In AI, success does not end the fundraising story. Sometimes it just makes the next chapter more expensive.

Why the Broader Market Makes This Even Trickier

Broad venture data tells an interesting story. Median dilution in many ordinary startup rounds has actually eased compared with the more painful reset years. AI leaders, meanwhile, are attracting a premium in valuation and round size. So if you looked only at median fundraising charts, you might conclude founders are doing better.

That is partly true. But the AI market is also becoming more concentrated. More capital is flowing into fewer, larger rounds. Late-stage liquidity remains limited, secondaries and tenders are rising, and equity grants have been under pressure in many companies. In plain terms, the market is friendlier for a small set of winners and still awkward for almost everyone else.

That concentration matters because mega-rounds distort intuition. A company can look wildly valuable and still be structurally fragile if it needs repeated financing to keep pace with model costs or platform competition. The cap table may be healthier than it would be at a lower valuation, but not healthy enough to justify complacency.

In AI, valuation often buys time. It does not always buy simplicity.

What Founders, Employees, and Early Investors Should Watch

If you are involved in an AI company, do not stop at the valuation headline. Ask the impolite but necessary questions.

- How much fresh primary capital is actually being raised?

- How much of the event is secondary and therefore non-dilutive?

- Is the option pool being increased before closing?

- What preferences or anti-dilution protections are attached to the new money?

- Will the company likely need another giant round in 12 to 24 months?

- Are governance rights shifting along with the stock economics?

- If the company restructures, who gains, who converts, and who gets squeezed?

These questions are not pessimistic. They are basic hygiene. You would not buy a house by only reading the real-estate headline and ignoring the inspection report. Do not do the venture equivalent just because the company uses the words “frontier” and “agents” a lot.

What This Feels Like on the Ground: of Real-World AI Deal Experience

Talk to people inside the AI funding machine and a pattern emerges. The valuation headline creates one emotional experience; the cap table creates another. Founders feel validated, then cautious. Employees feel rich, then confused. Investors feel lucky, then protective. Everyone smiles for the announcement post, and then somebody opens a spreadsheet.

For founders, the experience is often surreal. One month they are being told their startup is too early, too expensive, or too weird. The next month, once they have a believable AI story and a few credible enterprise customers, the room changes temperature. Suddenly the same investors who once wanted a modest round are asking whether the company is “thinking big enough.” Bigger round. Bigger valuation. Bigger talent plan. Bigger compute budget. Bigger dreams. The founder is flattered, of course. Then the legal drafts arrive, and the founder realizes “thinking bigger” can also mean “selling more of the future than expected.”

For employees, the experience is even stranger. AI companies often recruit with life-changing upside, and sometimes that upside is real. But private-market wealth is a funny thing. You can be “worth” millions on paper while still asking whether you should split the dinner check three ways. Employees see the valuation jump and assume their slice is doing the same. Sometimes it is. Sometimes new grants are smaller, refresh logic changes, or the company issues more shares than people realize. The number in the headline is public relations. The number that matters lives in the denominator.

Early investors tend to experience a mix of pride and paranoia. Pride, because backing an AI winner early is the kind of thing people casually mention for the rest of their natural lives. Paranoia, because giant financings attract giant expectations. New investors want rights. Strategic investors want influence. Later-stage money wants downside protection. A cap table that once looked elegant starts resembling an airport during a thunderstorm: crowded, delayed, and full of people asking for priority boarding.

Even boards feel the pressure differently in AI. In a normal software company, governance conversations often orbit growth, margins, and hiring. In an AI company, those topics are joined by safety, compute access, partnership dependency, and whether the company’s structure still matches its capital needs. That is why OpenAI matters so much as an example. It showed the whole market that in AI, the financing story and the governance story are often the same story wearing different clothes.

The lived experience, then, is not simply “AI makes people rich.” It is “AI accelerates everything”value creation, competition, urgency, hiring pressure, fundraising scale, and structural complexity. That is exciting. It is also exhausting. And it is why smart participants in this market celebrate the valuation, then immediately ask the least glamorous question in venture capital: “Great. Now who got diluted, how much, and in what way?”

Conclusion

AI dealmaking has entered the era of colossal numbers. But colossal valuations should not lull anyone into lazy analysis. In many cases, the higher the valuation, the bigger the underlying capital requirementand the more creative the structure needed to support it.

OpenAI shows the pattern clearly. Massive valuation? Yes. Massive growth? Also yes. But the public record around its fundraising, mission, governance, and evolving capital structure shows that private AI finance is not a fairy tale where everyone keeps their percentage and rides off into the cloud. It is a negotiation among ambition, control, infrastructure cost, and investor economics.

So the next time you see an AI startup raise money at a number large enough to frighten a calculator, resist the urge to stop reading after the valuation. Ask what was sold, what was restructured, what was promised, and what happens next. Because in AI, the headline may be about scale. The truth is usually in the dilution.