Table of Contents >> Show >> Hide

- What Gartner’s 2023 outlook actually signaled

- So why did SaaStr call it “even faster than we expected”?

- The forces that pushed SaaS spend up in 2023

- What changed inside the SaaS buying process in 2023

- Three concrete examples of how SaaS spend grows in a “tight” year

- What SaaS founders and operators should take from the 2023 “faster growth” narrative

- What buyers should do to stay sane while SaaS grows

- Field Notes: Real-World Experiences When SaaS Spend Accelerates (About )

- Conclusion: 2023 proved SaaS isn’t “extra”it’s infrastructure for modern work

In 2023, a lot of leaders tried to put software spend on a “healthy budget.” Fewer subscriptions. More approvals.

Maybe even a stern email titled “Unused Seats Will Be Rehomed”. And yet… SaaS spending still found a way

to grow. If that sounds like your organization, congratulations: you were not uniquely bad at saying “no.” You were

just living inside a big market reality.

SaaStr’s take on Gartner’s outlook landed because it captured a tension every operator felt: companies were getting

stricter about ROI, but demand for cloud-delivered software kept climbing anyway. The result was a year where

SaaS didn’t merely survive scrutinyit adapted to it, and in many categories it sped up.

What Gartner’s 2023 outlook actually signaled

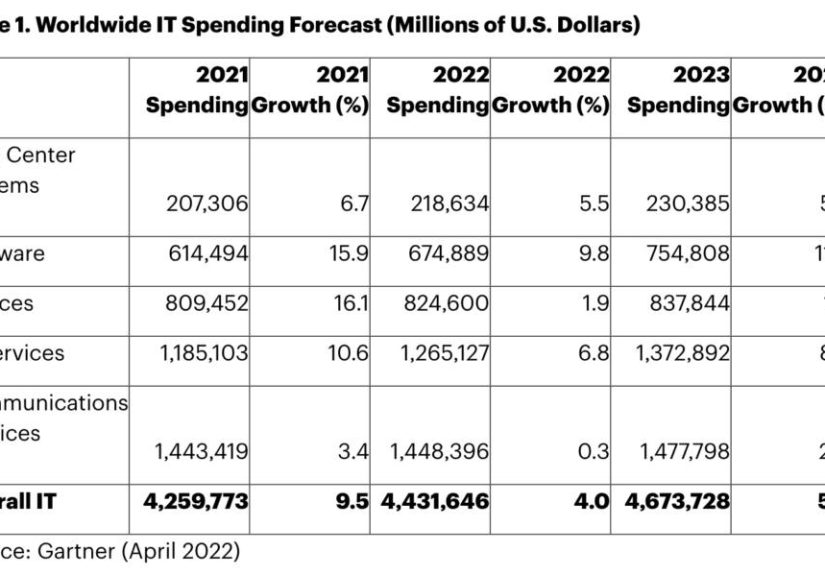

Gartner’s IT spending outlook heading into 2023 painted a surprisingly resilient picture: even with economic

turbulence, enterprise technology budgets were still oriented toward digital execution. In Gartner’s worldwide

IT spending forecast (released during the 2022 IT Symposium timeframe), software was projected to be one of the

stronger growth segments in 2023an important backdrop for why SaaStr framed the story as “faster than expected.”

Software growth: not a blip, a budget priority

Gartner projected worldwide software spending at roughly $879.6B in 2023, up from about

$790.4B in 2022, representing 11.3% growth. That’s not “nice to have” growth.

That’s “board asked what we’re doing about it” growth.

Public cloud services: SaaS remains the biggest slice

When people say “cloud spend,” they often picture infrastructure. But SaaS is the part of cloud that tends to show up

in the most departments, the most expense lines, and the most renewal calendars. Gartner’s public cloud services

tracking has consistently shown SaaS as a major segment, and later segment breakdowns reinforce that the SaaS portion

alone is in the hundreds of billions.

In plain English: even if a company slows hiring, it still needs CRM, HR, collaboration, security, finance, analytics,

support tools, and industry-specific software. Those are increasingly delivered as SaaSand those invoices do not

care about your feelings.

So why did SaaStr call it “even faster than we expected”?

SaaStr’s angle works because it matches how planning actually feels on the ground:

forecasts get revised, priorities shift, and software vendors keep shipping “must-have” featuresespecially where

security, compliance, and automation are concerned. Even when teams cut waste, the base demand stays strong.

A big theme in 2023 was this: cost discipline rose at the same time as dependency on SaaS rose.

That sounds contradictory until you watch what companies actually do. They don’t “stop SaaS.”

They optimize SaaSand then keep buying the tools that directly move revenue, reduce risk, or automate work.

The forces that pushed SaaS spend up in 2023

1) SaaS is the fastest path from problem to “fixed-ish”

In a year where leadership wanted speed and accountability, SaaS had a structural advantage:

it’s quicker to deploy than many on-premises alternatives, updates are continuous, and security posture is often

easier to centralize (even if vendor risk becomes a new homework assignment).

2) The “build vs. buy” debate evolved into “compose”

Many organizations didn’t choose between building everything and buying everything. They did both:

they bought platforms and tools, then composed workflows, automations, and integrations around them. That tends to

increase SaaS usage because it spreads software into operations, finance, customer support, and revenue teams.

3) Security and compliance spending didn’t take a year off

Security isn’t a “fun” line item, but it’s one of the least optional. In 2023, a lot of organizations treated

security tooling as a protective moat: identity, device management, endpoint protection, data controls, and

compliance monitoring. Many of those are delivered as SaaS subscriptions or SaaS-like services.

4) Cloud cost visibility became a sport (FinOps: the budget gym membership)

2023 was also a year where teams became more honest about waste. Cloud and SaaS sprawl turned into a CFO-friendly

storyline: “We can save money without breaking the business.” That pushed companies to invest in governance,

expense visibility, and cost optimization practicesoften under the umbrella of FinOps and procurement rigor.

The funny part is that cost optimization doesn’t always shrink the overall market. It often reallocates spend:

less on redundant tools and unused seats, more on high-usage platforms, integrations, and automation that keep

teams productive with fewer people.

What changed inside the SaaS buying process in 2023

Short version: renewals became negotiations

If 2021 was “sign the deal, we’ll figure it out later,” 2023 leaned toward “show me usage, show me outcomes,

and please explain why this costs more than my car.” Buyers asked tougher questions:

- Usage: Are people actually using this weekly, or is it just installed?

- Impact: Does it lift revenue, reduce churn, lower risk, or speed up delivery?

- Consolidation: Can this replace two other tools?

- Governance: Who owns renewal decisions, access, and offboarding?

- Security posture: What happens when (not if) something goes wrong?

But here’s the twist: tougher buying can still mean more spending

When buyers rationalize tools, the winners often expand. The “platform” vendors and mission-critical systems

may see larger, stickier contracts. Meanwhile, point solutions without clear ROI got squeezed.

Net result: the market grows, but the bar rises.

Three concrete examples of how SaaS spend grows in a “tight” year

Example 1: The revenue stack consolidation

A mid-market company decides it has “too many sales tools.” It cancels two smaller products,

but upgrades its core CRM and adds revenue intelligence, call recording, and forecasting.

Spend goes up even though tool count goes down.

Example 2: HR + finance modernization

Hiring slows, but HR operations get more complex: compliance, benefits, multi-country payroll,

and retention programs all matter more when you can’t hire your way out of problems.

The company invests in an HRIS upgrade and better analyticsSaaS spend rises because complexity rose.

Example 3: Security becomes a prerequisite for enterprise deals

A SaaS company selling to larger customers realizes that “we take security seriously” is not a plan.

They add SSO enforcement, device posture checks, logging, and compliance tooling.

That’s new software spend, but it’s directly tied to closing bigger contracts.

What SaaS founders and operators should take from the 2023 “faster growth” narrative

Design for scrutiny: ROI is a product feature now

In 2023, “nice UI” wasn’t enough. Winning SaaS products made it easy to prove value:

dashboards that show outcomes, admin controls that reduce waste, and reporting that supports renewal

conversations. If a champion can’t quantify impact, procurement will do it for them (and they’ll be meaner).

Pricing and packaging: align to how value is realized

Seat-based pricing can work, but only if seat count tracks value. Many buyers pushed back on unused access.

Value metrics that map to outcomesusage, volume, workflows, automations, transactionsbecame more compelling,

especially when paired with clear guardrails and forecasting.

Be the consolidator, not the “extra tab”

When companies rationalize stacks, they keep what replaces other tools.

That can mean building integrations, offering broader workflows, or partnering deeply with platforms.

The goal is to become a system customers can’t remove without causing pain (the professional, useful kind of pain).

What buyers should do to stay sane while SaaS grows

Create a living SaaS inventory (and stop pretending you’ll remember)

Most organizations don’t have a single owner for “all the SaaS.”

Finance sees invoices, IT sees access, business units see outcomes, security sees risk.

A basic inventoryapps, owners, users, renewals, contract terms, usagepays for itself quickly.

Make renewals boring (boring is good)

Renewals become chaos when they’re last-minute. A simple cadence helps:

120 days out: review usage and outcomes. 90 days out: renegotiate. 60 days out: decide. 30 days out: execute.

Boring renewals reduce surprise spend and prevent “auto-renewal oopsies.”

Invest in cost governance without killing innovation

The best approach is not “no tools.” It’s “tools with accountability.” Central standards for security and

procurement can coexist with fast team experimentationif you have clear owners, tagging, and offboarding.

Field Notes: Real-World Experiences When SaaS Spend Accelerates (About )

When SaaS spending grows faster than expected, it rarely feels like a single dramatic decision. It feels like a

hundred small oneseach rational in isolation, collectively powerful.

One common experience is the “consolidation paradox.” Teams start the year convinced they’ll reduce tools by 20%.

They do cut a few: that rarely used social scheduler, the duplicate project tracker, the random analytics add-on

bought during a late-night panic. Everyone celebrates. Then the organization upgrades the tools that remain.

The CRM becomes the CRM-plus-everything hub. The help desk becomes a full customer platform with automation,

knowledge base, and AI-assisted routing. The collaboration suite expands into whiteboarding, webinar tooling,

and advanced security. Tool count goes down, but the winners expand into bigger contracts. The net spend? Often flat

to upbecause the business still demands capability, just with fewer moving parts.

Another recurring experience is that “budget tightening” mostly means “budget justification.” In practice, that

changes the conversations inside companies. Champions stop pitching features and start pitching outcomes:

reduced time-to-close, fewer support tickets per customer, faster onboarding, lower security risk, quicker release

cycles. The best internal pitches include screenshots of usage, simple before/after metrics, and a clear narrative

of what breaks if the tool disappears. In 2023, that style of internal selling became normal. The organizations that

couldn’t tell the value story didn’t necessarily stop buying software; they just bought software with better

evidence.

A third pattern is “seat hygiene” becoming a habit. Companies that never cared about access suddenly cared a lot.

Offboarding became sharper. Department heads got monthly usage reports. Some teams implemented role-based licensing

(power users vs. occasional users) or shifted users to cheaper tiers. This doesn’t kill spendit reallocates it.

It can even fund new purchases: “We saved $40K by cleaning up licenses; we can afford the security upgrade now.”

It’s the same money moving toward higher-priority software.

Finally, many teams experienced the “integration reality check.” As SaaS ecosystems expand, the pain isn’t only

subscriptionsit’s stitching tools together. In 2023, organizations often discovered that the real cost of a tool

includes admin time, data quality, integration work, and security reviews. That experience pushes buyers toward

platforms, strong APIs, and vendors that make integration less painful. Vendors that reduce operational friction

often win expansions, because they save the one resource every team is short on: attention.

Conclusion: 2023 proved SaaS isn’t “extra”it’s infrastructure for modern work

The big takeaway from Gartner’s outlook (and SaaStr’s punchy framing) is not simply that SaaS spending grew.

It’s why it grew: businesses kept prioritizing digital execution, and SaaS is where strategy becomes

operational reality. 2023 made buyers sharper and vendors more accountablebut it didn’t reverse the direction of

the market. It made the market more selective, more ROI-driven, and (in many categories) still faster than expected.