Table of Contents >> Show >> Hide

- What Is the Average Credit Card Debt Per Household in the U.S.?

- Why Different Sources Give Different Credit Card Debt Numbers

- Why Credit Card Debt Has Been Rising

- How Interest Rates Make Credit Card Debt Feel Heavier

- Is Your Credit Card Debt Above or Below Average?

- Signs Credit Card Debt Is Becoming a Problem

- Average Credit Card Debt by Age and Life Stage

- How Credit Card Debt Affects Household Finances

- How to Pay Down Credit Card Debt Faster

- How Much Credit Card Debt Is Too Much?

- Experience-Based Insights: What Credit Card Debt Feels Like in Real Life

- Conclusion

Credit card debt is one of those financial topics that can make people suddenly very interested in cleaning the garage. It sounds heavy, a little stressful, and possibly expensive. But understanding the average credit card debt per household is not about judging anyone’s wallet. It is about getting a clear picture of where American families stand, why balances keep rising, and what a realistic payoff plan can look like.

So, how much is the average credit card debt per household? The most useful answer depends on how you define “average.” If you divide total U.S. credit card balances by all American households, the figure lands around the mid-to-high $9,000 range using recent national data. But if you look only at households that actually carry revolving credit card debt from month to month, the average is higher: about $11,000 per indebted household. Meanwhile, credit bureau data often reports average debt per borrower, which is closer to the $6,500 to $6,700 range.

In other words, the “average” is not one magic number. It is more like a financial group chat: several numbers are talking at once, and you need to know who is speaking.

What Is the Average Credit Card Debt Per Household in the U.S.?

Recent U.S. household debt reports show that total credit card balances have reached record levels, with Americans owing roughly $1.28 trillion in credit card debt by the end of 2025. That number includes balances across millions of accounts, including people who pay in full and people who carry balances month to month.

Using the estimated number of U.S. households, total credit card balances divided across all households would produce an average near $9,500 per household. However, that broad number can be misleading because not every household has credit card debt. Some people have no credit cards, some use cards only for rewards and pay them off every month, and others carry balances for years.

A more practical measure is the average revolving credit card debt among households that carry balances. Revolving debt means debt that rolls from one billing cycle into the next and typically accrues interest. By that measure, recent estimates put the average household credit card debt at about $11,149 among households with revolving credit card debt.

Why Different Sources Give Different Credit Card Debt Numbers

If you have ever searched “average credit card debt per household” and found five different answers, congratulations: you have met the wonderful world of financial methodology. Not all credit card debt statistics measure the same thing.

Average Per Household

This method divides total credit card debt by the number of households. It is simple, but it spreads debt across everyone, including households with no credit card debt at all.

Average Per Household With Debt

This is often more useful for real-life comparison. It looks only at households that carry credit card balances. Because the denominator is smaller, the average is higher.

Average Per Borrower

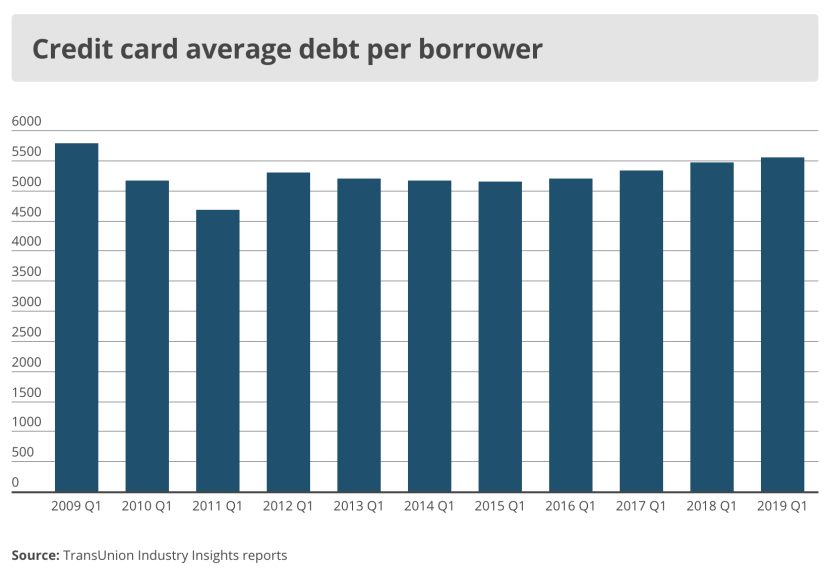

Credit bureaus and lenders often use borrower-level data. This measures the average balance among people with credit card debt or open credit card accounts. Recent borrower-level estimates are commonly around $6,500 to $6,700.

Total National Credit Card Debt

This is the big headline number. When you see that Americans owe around $1.28 trillion on credit cards, that is total national credit card debt. It is useful for tracking the economy, but it does not tell you what one household owes.

Why Credit Card Debt Has Been Rising

Credit card debt has climbed for several reasons, and none of them are as simple as “people bought too many fancy coffees.” Sure, impulse spending exists. But the larger picture includes inflation, housing costs, medical bills, car repairs, higher interest rates, and wages that do not always keep up with household expenses.

For many families, credit cards have become a short-term bridge between income and expenses. Groceries, gas, insurance premiums, school supplies, pet emergencies, and surprise dental bills do not wait politely until payday. Credit cards can help cover the gap, but if the balance is not paid off quickly, interest turns that bridge into a toll road.

Another factor is the popularity of rewards cards. Many Americans use credit cards for points, cash back, travel miles, and purchase protection. Used wisely, those perks can be valuable. But rewards lose their sparkle fast when a cardholder carries a balance at an interest rate above 20%.

How Interest Rates Make Credit Card Debt Feel Heavier

Credit card debt is not just about the amount borrowed. It is also about the cost of carrying that amount. Recent Federal Reserve data shows average credit card interest rates around 21% for all accounts, and many consumers with lower credit scores pay even higher rates.

Here is a simple example. Suppose a household carries a $7,000 credit card balance at a 21% annual percentage rate. If the household pays only a small amount each month, a large share of each payment goes toward interest instead of reducing the balance. That is why minimum payments can feel like running on a treadmill while the treadmill sends you a bill.

Paying more than the minimum can dramatically reduce interest charges. Even an extra $50 or $100 per month can shorten the payoff timeline and save hundreds or thousands of dollars. The key is consistency, not perfection.

Is Your Credit Card Debt Above or Below Average?

If your household credit card debt is below $5,000, you may be below many national averages, especially compared with households that carry revolving balances. If your debt is around $10,000 to $12,000, you are close to the average for households with revolving credit card debt. If your balances are above $15,000 or $20,000, you are not alone, but it may be time to create a focused payoff strategy.

Still, averages do not tell the whole story. A $6,000 balance may be manageable for a household with strong income, low fixed expenses, and a clear repayment plan. The same balance may be overwhelming for someone dealing with job loss, medical costs, or rising rent. The better question is not only “How do I compare?” but “Can my budget safely handle this debt?”

Signs Credit Card Debt Is Becoming a Problem

Credit card debt becomes risky when it starts controlling your monthly cash flow. Watch for signs such as paying only the minimum every month, using one card to pay another bill, relying on credit cards for basic expenses, missing due dates, or feeling anxious every time a statement arrives.

Another warning sign is a rising credit utilization ratio. Credit utilization is the percentage of available credit you are using. For example, if you have a $10,000 credit limit and a $5,000 balance, your utilization is 50%. High utilization can hurt your credit score and make future borrowing more expensive.

Debt also becomes more dangerous when there is no payoff date. If you do not know when your balance will hit zero, the debt can feel permanent. A payoff calculator, spreadsheet, or budgeting app can turn a vague problem into a specific plan.

Average Credit Card Debt by Age and Life Stage

Credit card debt also varies by age. Younger adults may have lower balances because they have had less time to build credit limits, but they may also face student loans, entry-level wages, and high rent. Middle-aged households often carry higher balances because they may be juggling mortgages, childcare, aging parents, car loans, and college expenses. Older adults may carry less credit card debt on average, but fixed retirement income can make even smaller balances stressful.

Generation X often shows some of the highest average credit card balances. That makes sense when you consider the “sandwich generation” effect: many are supporting children, helping parents, maintaining homes, and trying to save for retirement at the same time. That is not a budget; that is an Olympic event with receipts.

How Credit Card Debt Affects Household Finances

Credit card debt affects more than your monthly payment. It can influence your credit score, loan approval odds, mortgage rates, insurance costs, and ability to save. A household paying hundreds of dollars per month toward credit card interest has less money for emergency savings, retirement contributions, vacations, or replacing the washing machine before it starts making helicopter noises.

The emotional cost matters too. Debt can create stress, reduce sleep quality, and make normal purchases feel loaded with guilt. Many households carry credit card debt quietly because they assume everyone else is doing better. In reality, millions of Americans are managing similar balances. The goal is not shame. The goal is a plan.

How to Pay Down Credit Card Debt Faster

1. Stop Adding New Debt When Possible

The first step is to slow the leak. If you keep using the same card while trying to pay it off, progress becomes harder to see. Consider using a debit card or cash for daily spending while focusing on repayment.

2. Choose a Payoff Method

The debt snowball method focuses on paying off the smallest balance first for quick wins. The debt avalanche method focuses on paying off the highest-interest balance first to save the most money. Both can work. The best method is the one you will actually follow after a long day when takeout sounds like a personality trait.

3. Pay More Than the Minimum

Minimum payments keep accounts current, but they are not designed to make debt disappear quickly. Adding extra money to the principal balance can reduce interest and shorten the payoff timeline.

4. Consider a Balance Transfer

A balance transfer card with a 0% introductory APR can help if you qualify and have a realistic plan to pay down the balance before the promotional period ends. Watch for transfer fees and avoid treating the new card as fresh spending room.

5. Talk to a Nonprofit Credit Counselor

If the debt feels unmanageable, a nonprofit credit counseling agency may help you review your budget and explore options such as a debt management plan. This can be especially useful if multiple cards are involved.

How Much Credit Card Debt Is Too Much?

There is no single dollar amount that is automatically “too much.” A better rule is to compare debt payments with income and essential expenses. If credit card payments prevent you from building even a small emergency fund, paying rent or mortgage comfortably, buying groceries, or saving for basic goals, the debt is probably too high for your current budget.

Another useful benchmark is utilization. Keeping credit utilization below 30% is often recommended for credit health, and lower is usually better. If your cards are close to maxed out, lenders may see you as a higher-risk borrower, even if you have never missed a payment.

Experience-Based Insights: What Credit Card Debt Feels Like in Real Life

On paper, average credit card debt per household looks like a clean statistic. In real life, it looks like a family deciding whether to pay the card or fix the car. It looks like a parent buying school clothes in August and promising to “catch up” by October. It looks like a couple moving a balance from one card to another and realizing the old card still has the grocery store saved in the app.

One common experience is the slow build. Very few households wake up one morning and suddenly owe $11,000. More often, debt arrives in small, reasonable-looking pieces. A $300 car repair goes on the card. Then a $600 medical bill. Then a holiday trip, a broken phone, higher grocery costs, and a month where overtime disappeared. Each charge seems manageable alone. Together, they form a balance that feels like it brought luggage.

Another familiar experience is minimum-payment fatigue. At first, making the minimum feels responsible because the account stays current. But after several months, the balance barely moves. The statement says you paid, your bank account agrees, and yet the debt sits there like a houseguest who does not understand hints. This is where many people realize that credit card interest is not just a number. It is a force that slows progress unless you pay extra.

Many households also experience debt guilt. They compare themselves with friends, neighbors, or social media strangers who appear to have flawless kitchens, perfect vacations, and no financial stress. But credit card debt is often invisible. The family with the shiny vacation photos may be carrying a balance too. The person driving the newer car may be juggling payments behind the scenes. Comparing your private budget to someone else’s highlight reel is a fast way to feel worse and learn nothing useful.

The most encouraging experience is the first month of real progress. It may not be dramatic. Maybe the balance drops from $8,200 to $7,950. Maybe one small card is paid off. Maybe you finally know your debt-free date. That first visible win matters because it changes the story from “I am stuck” to “This is moving.” Debt payoff is rarely glamorous, but it is deeply satisfying. It turns financial stress into a checklist, and every checked box gives you a little more breathing room.

People who successfully pay down credit card debt often say the biggest change was not mathematical. It was behavioral. They checked balances weekly, planned purchases before swiping, used automatic payments, built a starter emergency fund, and stopped pretending the debt would fix itself. No magic wand appeared. No budgeting fairy landed on the windowsill. But small habits, repeated long enough, did what panic could not.

Conclusion

The average credit card debt per household depends on the measurement used. Across all households, the average is roughly around the mid-to-high $9,000 range based on total national credit card balances and household counts. Among households that carry revolving credit card debt, the average is closer to $11,149. Borrower-level averages are lower, commonly around $6,500 to $6,700.

The most important takeaway is not whether your balance is above or below average. It is whether your debt has a clear payoff plan, a manageable monthly payment, and a shrinking balance. Credit card debt is common, but it does not have to be permanent. With a focused strategy, extra payments, lower-interest options, and better spending habits, households can turn a stressful balance into a finished chapter.

Note: Debt statistics vary by source and methodology. This article uses rounded figures from recent U.S. household debt, credit bureau, consumer finance, and federal data. Readers should treat averages as educational benchmarks, not personal financial advice.