Table of Contents >> Show >> Hide

- From Big Promises to Legal Roadblocks

- What Polls Say About Student Loan Forgiveness Now

- Forgiveness Is Happening Just Not the Way Many Imagined

- Why the Public Thinks Broad Forgiveness Is Less Likely

- How Borrowers Are Adapting to Slimmer Chances of Forgiveness

- Practical Moves When You’re Not Counting on Student Loan Forgiveness

- Real-World Experiences: Living With Slimmer Odds of Student Loan Forgiveness

- The Bottom Line: Less Hype, More Strategy

A few years ago, “student loan forgiveness” felt like more than a slogan. It was a headline, a campaign promise, and for millions of borrowers, a lifeline. Then came court challenges, political battles, and a lot of confusing policy acronyms. Today, the mood is noticeably different: Americans still care about student debt, but many no longer believe sweeping forgiveness is actually going to happen.

Polls show support for some form of student loan relief, yet confidence that the federal government will erase big chunks of debt has faded. At the same time, billions of dollars are being forgivenjust through a maze of smaller, targeted programs that are hard to follow and even harder to qualify for.

In this deep dive, we’ll unpack why the public sees a slimmer chance of student loan forgiveness, what’s really happening behind the scenes, and how borrowers are adjusting their expectations and strategies in a post-“big cancellation” era.

From Big Promises to Legal Roadblocks

The rise and fall of mass cancellation

The modern debate over student loan forgiveness exploded when the federal government proposed canceling up to $10,000 in federal student loans for most borrowers, and up to $20,000 for those who had received Pell Grants. Tens of millions of people were told they might qualify, and millions were conditionally approved before any money was actually wiped away.

Then came the Supreme Court. In 2023, the Court struck down that sweeping forgiveness plan, ruling that the administration had exceeded the authority granted under a pandemic-era law. That decision was more than a legal setback; it was a psychological one. For many borrowers, the message was: “If they couldn’t pull this off at the peak of public attention, what are the odds now?”

Subsequent attempts to provide relief through different legal pathways have also run into headwinds, including additional court orders pausing or limiting parts of newer relief efforts and repayment plans. Each new legal challenge reinforces the perception that broad, across-the-board forgiveness is a long shot rather than a sure thing.

Why borrowers feel “once bitten, twice shy”

When you’re told your balance may drop by thousands of dollars, then watch that promise get reversed in court, it changes how you think about your loans. Many borrowers applied, waited, and celebratedonly to find themselves right back where they started, except with more anxiety and a renewed monthly bill after the pandemic payment pause ended.

That “whiplash” effect matters. Even when policymakers roll out new proposals, a lot of people mentally file them under “I’ll believe it when I see it.” The result: support for relief may still exist, but expectations of sweeping forgiveness have gotten much more cautious.

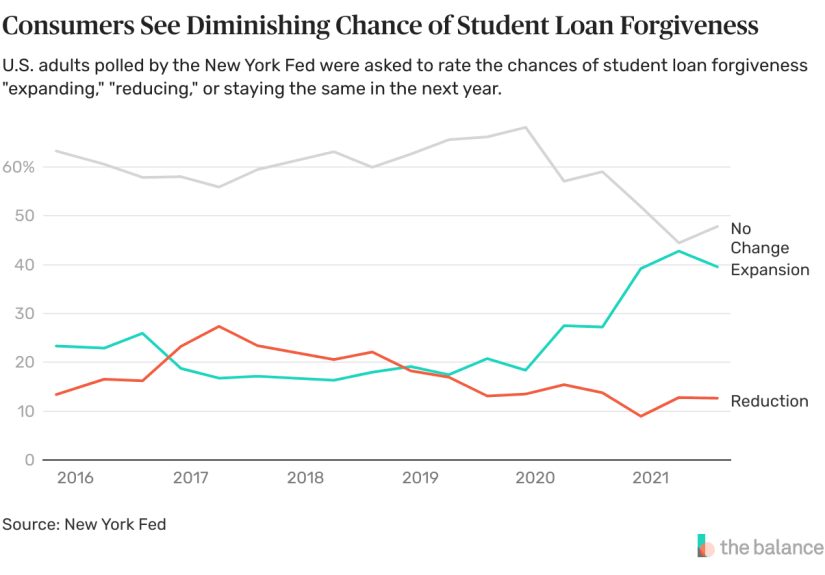

What Polls Say About Student Loan Forgiveness Now

Public opinion on student loan forgiveness is nuanced. It’s not that Americans suddenly don’t care; it’s that the issue competes with many other financial pressures and is deeply shaped by partisanship and personal experience.

Recent polling from academic and research groups finds:

- Less than half of U.S. adults say it is “extremely” or “very” important for the federal government to forgive student loan debt. In one national poll, that figure was around four in ten adults, and people ranked medical debt relief as a higher priority than student debt relief.

- The importance of forgiveness is strongly tied to partisanship. Democrats are much more likely than Republicans to say student debt relief should be a key federal priority, with independents landing somewhere in the middle.

- People who currently have student loansor are helping pay someone else’sare far more likely to call the issue a “crisis” and to say it influences how they vote, compared with those who never had loans or have already paid them off.

At the same time, other surveys show that a solid majority of Americans support some type of relief when it is framed as helping borrowers who are struggling financially or who have been in repayment for many years. Voters may be skeptical about a giant, one-time cancellation, but they aren’t indifferent to the pressure student loans create.

The bottom line from the polling: support for relief is still there, but faith that large-scale forgiveness will actually happen is weaker. Instead of expecting a dramatic wipeout, the public increasingly assumes that any help will be slower, narrower, and more conditional.

Forgiveness Is Happening Just Not the Way Many Imagined

Here’s the twist: while big, headline-grabbing cancellation has stalled, the federal government is still forgiving a lot of student debt through existing and updated programs.

Data compiled from federal reports show that hundreds of thousands of borrowers have seen their loans discharged through:

- Public Service Loan Forgiveness (PSLF): After years of criticism about sky-high denial rates, temporary waivers and new rules have helped more public service workers finally get the forgiveness they were promised.

- Income-driven repayment (IDR) account adjustments: Borrowers in long-term repayment, especially those who have been making payments for decades, have had past payments re-counted, leading to immediate cancellation for some.

- Borrower defense and school-related discharges: People who attended schools that misled them or abruptly closed have received group discharges worth billions of dollars.

By some estimates, federal efforts over the past several years have already canceled well over $100 billion in student loans for millions of borrowers, even as courts blocked the single large omnibus plan. Yet these discharges often happen quietly and in waves. There’s no single dramatic moment where everyone’s balance drops at onceso to the average borrower, it can feel like “no forgiveness is happening,” even while many others are benefiting.

This mismatch between reality and perception fuels the sense that forgiveness is unlikely. If you don’t fit into one of the “targeted” categories, you may feel forgotten, even while the government points to big cumulative numbers of forgiven debt.

Why the Public Thinks Broad Forgiveness Is Less Likely

Repeated court battles

The legal landscape is a major reason optimism has cooled. The Supreme Court has already rejected one massive forgiveness plan, and additional relief strategies have run into lawsuits, injunctions, or temporary blocks. Parts of newer repayment and forgiveness policies have been put on hold by federal courts, leaving borrowers once again in limbo.

When every bold idea is immediately challenged, the public naturally assumes that any large-scale cancellation effort will be tied up in court for yearsor quietly abandoned.

Deep political polarization

Student loan forgiveness has become a highly partisan issue. Many Republicans argue that large-scale cancellation is unfair to people who didn’t go to college, paid off their loans, or chose less expensive options. They also raise concerns about cost, inflation, and executive overreach.

Many Democrats and advocacy groups, meanwhile, see forgiveness as a tool to correct decades of rising tuition, wage stagnation, and racial wealth gaps. They argue that the government has been very generous in forgiving other kinds of obligationslike certain business loans or tax breakswhile being strict about educational debt.

This divide makes durable, bipartisan legislation on broad cancellation unlikely. Instead, most changes come through regulation and executive action, which are easier to undo when power shiftsand more vulnerable to legal challenges. Voters see this tug-of-war and conclude that nothing sweeping is “safe” or permanent.

Confusing rules and high denial rates

Even where forgiveness programs exist, they can be painfully complex. For years, borrowers applying for PSLF or other kinds of relief faced denial rates that were stunningly high, often because of technicalities like the wrong loan type, the wrong repayment plan, or missing documentation.

Although some of those rules have been relaxed and more borrowers are getting approved, the memory of “Sorry, you don’t qualify” letters lingers. When people see headlines about high denial rates or hear friends’ horror stories, they assume they’ll be shut out, too. That feeds the perception that real-world forgiveness is rareeven when the total number of forgiven loans is growing.

How Borrowers Are Adapting to Slimmer Chances of Forgiveness

As the hope of a once-and-for-all cancellation fades, borrowers are shifting from “maybe it’ll disappear” to “I need a strategy.” Surveys conducted after the pandemic payment pause ended show many borrowers struggling to restart payments, but also actively searching for ways to manage their debt.

Common adaptations include:

- Leaning into income-driven repayment (IDR): Many people are enrolling in IDR plans that cap payments as a share of income, even if they don’t entirely trust the eventual forgiveness provisions. For borrowers with modest incomes, these plans can reduce monthly payments significantly, even if long-term forgiveness remains uncertain.

- Rethinking further education: Some potential graduate students are reconsidering high-cost programs, especially in fields where earnings are uncertain. Others are choosing lower-cost institutions, in-state schools, or shorter programs to limit future debt.

- Using employer assistance: A growing number of employers, especially larger companies and public-sector organizations, offer student loan repayment benefits or separate tuition assistance. Borrowers who no longer believe in a giant federal bailout are more motivated to squeeze every dollar out of these programs.

- Prioritizing financial resilience: Instead of throwing every spare dollar at their loans, some borrowers are splitting effortsbuilding an emergency fund or retirement savings while keeping student loans in a manageable repayment plan. The logic: if massive forgiveness isn’t coming, long-term financial stability matters more than racing to zero at all costs.

None of these strategies are perfect, and many borrowers still feel squeezed. But the overall mindset is shifting from waiting for a miracle to navigating a long-term reality.

Practical Moves When You’re Not Counting on Student Loan Forgiveness

If you’re operating on the assumption that broad forgiveness probably isn’t coming soonif at allthere are still ways to put yourself in the best possible position.

1. Map your loans and your options

Start with a clear inventory: federal vs. private loans, balances, interest rates, and current repayment plans. Many borrowers don’t realize certain protections and forgiveness options only apply to federal loans. Knowing exactly what you have makes it easier to see which programs might help you, from PSLF to income-driven plans to targeted relief for long-term repayment or financial hardship.

2. Match your repayment plan to your reality

The “right” plan depends on income, family size, and goals:

- If you work in government or qualifying nonprofits, combining PSLF with an income-driven plan may be more valuable than aggressively paying down principal.

- If you’re in a high-paying field and don’t expect to qualify for any forgiveness, a standard or accelerated plan could minimize total interest, especially if you can make extra payments.

- If your income is unstable or relatively low, an IDR plan that ties payments to earnings may reduce stress, even if the loan lasts longer.

The key is to choose intentionally, instead of defaulting into the first plan you were assigned.

3. Look beyond Washington

State-based programs, employer benefits, and profession-specific incentives can quietly chip away at your balance. Teachers, nurses, social workers, and other public-service professionals sometimes qualify for state or local repayment help. Some hospitals, school districts, and private employers now promote loan repayment support alongside 401(k) matches and health insurance.

None of these are as dramatic as a giant federal cancellation, but they can make a meaningful difference over timeespecially when combined with smarter repayment choices.

4. Protect your financial mental health

One under-discussed side effect of the forgiveness roller coaster is emotional exhaustion. Many borrowers feel whipsawed between hope and disappointment. Accepting that the system changes slowly (and often messily) can help you focus on what you can control: your budget, your plan, and your long-term priorities.

Student loans may be a big piece of your financial puzzle, but they’re not the whole picture. Building savings, improving job skills, and planning for retirement matter, tooespecially if major forgiveness is no longer the centerpiece of your strategy.

Real-World Experiences: Living With Slimmer Odds of Student Loan Forgiveness

To understand how shifting expectations play out in real life, imagine three borrowers whose stories echo what many people are going through.

Case study #1: The public school teacher

Maya, a middle-school teacher, graduated with roughly $60,000 in federal loans. When broad student loan cancellation was first announced, she ran calculators, dreamed about finally buying a home, and told her parents she might be debt-free years earlier than expected. When the decision was struck down, she felt more let down than she expectedalmost embarrassed she had allowed herself to hope.

Instead of giving up, she doubled down on programs that actually fit her life. She confirmed that her school qualifies for Public Service Loan Forgiveness, switched to an income-driven plan that kept her monthly payment manageable, and set up automatic employment certification each year. Forgiveness still isn’t guaranteed, and it will take time, but she now treats PSLF like a long-term benefit of her careersimilar to a pension or retirement matchrather than a windfall.

Case study #2: The mid-career parent

Alex is in his 40s, juggling work, a mortgage, and kids. He had nearly written off his own student loans as “just another bill” when the big cancellation headlines hit. For the first time, he thought, “Maybe this really will disappear.” When it didn’t, the disappointment stungbut it also pushed him to re-evaluate his overall finances.

Instead of throwing everything at the loans, Alex made a different choice: he kept his payment steady on an income-driven plan and focused on building an emergency fund and increasing his retirement contributions. He doesn’t expect sweeping forgiveness anymore, but he does expect his future self to be better protected. The debt is still there; the difference is that it no longer controls every other financial decision.

Case study #3: The recent graduate

Jordan graduated right as payments were restarting. They had watched older friends talk about promised forgiveness that never fully materialized and didn’t want to build their entire plan around something that might get overturned again.

From day one, Jordan treated forgiveness as a “maybe” and repayment as a “definitely.” They chose a lower-cost apartment, picked up a side gig to smooth out income, and set their loans on auto-debit to avoid missed payments. When they learned about targeted relief for long-term borrowers and financial hardship, Jordan mentally filed that under “bonus potential,” not “Plan A.”

The common thread in all three stories isn’t resignationit’s realism. Borrowers can still support forgiveness efforts, vote their values, and hope for better policies. But day-to-day, they’re building plans that work even if the big, headline-grabbing cancellation never arrives.

The Bottom Line: Less Hype, More Strategy

The public’s view of student loan forgiveness has shifted from “it’s coming” to “don’t count on it.” Polls show that while many Americans still support some form of relief, they rank it against other priorities and increasingly doubt that sweeping cancellation will survive legal and political battles anytime soon.

At the same time, real forgiveness is happening in the background through PSLF, income-driven repayment adjustments, borrower defense, and targeted hardship programs. The catch is that these forms of relief are narrower, slower, and more complicated than a one-time across-the-board wipeout.

For borrowers, that reality calls for a mindset shift. Instead of waiting for a miracle headline, it’s smarter to:

- Understand which programs you actually qualify for.

- Choose repayment plans that protect your budget and long-term goals.

- Take advantage of employer and state-level help where it’s available.

- Advocate for better policy, but build a financial life that doesn’t depend on it.

The odds of giant, universal student loan forgiveness may be slimmer than they once seemed. But with clear information, realistic expectations, and a bit of strategy, borrowers can still move toward financial stabilityeven if the promised magic wand never appears.