Table of Contents >> Show >> Hide

- What Is “The Biggest Problem in Finance” Anyway?

- The Asset Ownership Gap: Why the Rich Get Richer

- The Knowledge Gap: Financial Literacy Is Still Shockingly Low

- Behavioral Biases: Why We Sabotage Ourselves

- Retirement Reality Check: Shortfalls Everywhere

- So What’s the Real “Biggest Problem in Finance”?

- Practical Ways to Fight Back (Without Becoming a Finance Nerd)

- Real-World Experiences: How This Plays Out in Everyday Life

- Conclusion: Common Sense as a Superpower

If money really made sense, we wouldn’t have to Google “How much do I need to retire?” at 2 a.m. while stress-eating cereal.

Yet here we are. Despite more financial apps, low-cost index funds, and personal finance blogs than ever, most people still feel

behind. So what is the biggest problem in finance?

Spoiler: it’s not that compound interest is too complicated or that you’re bad at math. The real problem is a mix of

who owns financial assets, how people behave with money, and how little financial literacy most households actually have.

In other words, the system and our human wiring are out of sync.

Inspired by the ideas behind A Wealth of Common Sense, let’s unpack why the rich keep getting richer,

why the middle class often feels stuck, and what you can dopracticallyto stop feeling like finance is an exam

you somehow missed the class for.

What Is “The Biggest Problem in Finance” Anyway?

At a high level, here’s the core issue:

- The wealthiest households own most of the productive financial assetsstocks, bonds, business equity.

- The typical middle-class household’s biggest asset is their home, plus maybe a small retirement account.

- Meanwhile, financial literacy is low, behavioral biases are strong, and retirement systems are confusing.

That combination creates a finance world where markets can soar, corporate profits can rise, and yet huge chunks of the population

don’t fully benefit. The problem isn’t just inequality in incomeit’s inequality in

how people participate in the financial system.

The Asset Ownership Gap: Why the Rich Get Richer

Who Actually Owns the Stock Market?

Research cited by A Wealth of Common Sense shows that the top 10% of households by wealth own the vast majority of the U.S. stock market.

Their slice is estimated at well over 80% of equities, and only about half of American households own any stock at all,

even via retirement accounts.

Think about what that means: when the S&P 500 has a decade-long run, most of the gains flow to people who were already wealthy.

The stock market isn’t brokenit’s just that many households aren’t actually in the game in a meaningful way.

Meanwhile, surveys from regulators and financial institutions repeatedly show that a significant share of Americanssometimes as high as

20–46%have no retirement savings at all. That’s not a market problem. That’s an access and participation problem.

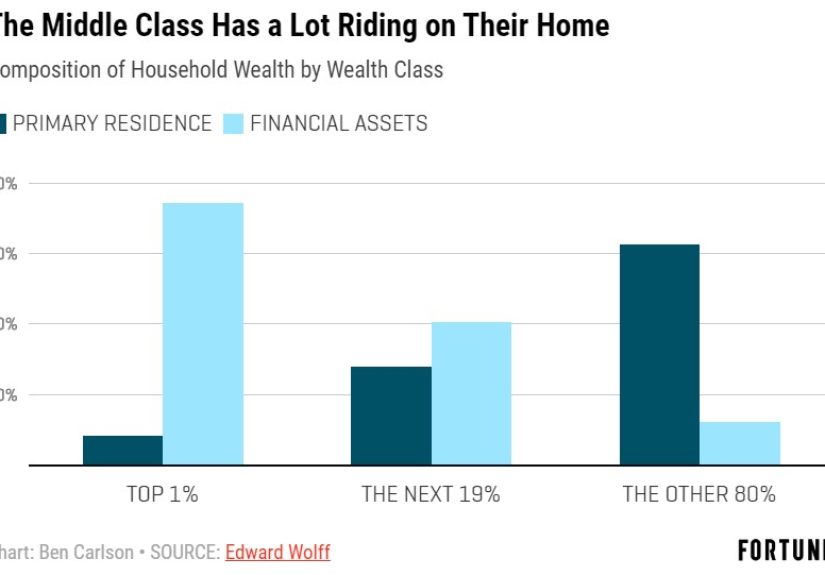

Housing Heavy, Financial Assets Light

The original “Biggest Problem in Finance” essay points out another uncomfortable truth: the wealthy own diversified financial assets;

the middle class often has almost everything tied up in a single home.

On paper, a house looks like a great investment story: buy, hold, hopefully sell higher. In reality, housing is a strange hybrid:

- Asset: it can appreciate over time.

- Liability: you take on a mortgageoften your biggest debt.

- Consumption: you live in it, maintain it, remodel the kitchen when Instagram convinces you your cabinets are shameful.

U.S. household debt is dominated by mortgagesroughly two-thirds to 70% of total household debt in many data sets.

That means a huge portion of the middle class is simultaneously:

- Highly leveraged into one illiquid asset.

- Under-invested in diversified financial markets.

The wealthy, by contrast, can own real estate and large portfolios of stocks, bonds, and business interests.

When markets rise, their net worth grows faster and more consistently.

The Knowledge Gap: Financial Literacy Is Still Shockingly Low

You’d think that in a world of free investing blogs, YouTube channels, and robo-advisors, financial literacy would be soaring.

Not exactly.

Multiple major surveys paint a similar picture:

-

A long-running U.S. financial literacy index finds that the average adult answers only about half of basic personal finance questions correctly,

and scores have slightly declined in recent years. -

Only about 19% of U.S. adults say they took a dedicated personal finance class in high school, and fewer than 30 states

require such a course to graduate. - Other surveys show that only around a quarter of adults can correctly answer most basic personal finance knowledge questions.

In simple terms: we’ve built a financial system that requires people to make complex decisions about investing, debt, insurance,

and retirementbut we haven’t consistently taught them how any of it works.

That’s like handing everyone a car with a manual transmission, tossing them the keys, and saying, “Good luck, try not to stall on the highway.”

Behavioral Biases: Why We Sabotage Ourselves

Even for people who do understand the basics, human psychology often gets in the way. Behavioral finance research shows that investors

don’t act like perfectly rational robots; they act like humans with emotions, stories, and biases.

Loss Aversion

Losing hurts more than winning feels good. That’s loss aversion. It can cause investors to:

- Refuse to sell losing investments, hoping they’ll “come back.”

- Sell winning investments too early to “lock in” gains.

- Avoid investing in stocks at all after a painful loss.

Over time, this behavior often produces the opposite of what people want: higher risk with lower returns.

Overconfidence and Herd Mentality

Many investors believe they’re better than average at picking stocks, timing the market, or spotting the next hot asset.

Statistically, we can’t all be above averagebut try telling that to someone who just got lucky on a tech stock.

Add herd mentality (buying because “everyone else is making money there”) and recency bias (assuming that whatever happened recently

will keep happening), and you get classic boom-and-bust cycles. People pile in after big gains and panic-sell after big dropsbuying high

and selling low, over and over.

Familiarity and Anchoring

People also tend to:

- Stick with familiar companies or industries, creating concentrated portfolios.

- Anchor on past prices (“I’ll sell when it gets back to my purchase price”), even when the fundamentals have changed.

None of these behaviors are “dumb.” They’re human. But when combined with low financial literacy and a complex system,

they quietly erode long-term wealth.

Retirement Reality Check: Shortfalls Everywhere

Retirement is where all these problems collide: asset ownership, literacy, and behavior.

Recent data from major financial institutions and research organizations show:

- Somewhere between 20% and 46% of Americans have no retirement savings.

-

Many Americans believe they’ll need roughly $1.2–$1.3 million to retire comfortably, yet a large portion have only a fraction

of that saved. - Around half of people nearing retirement say they’re not confident their savings will last their lifetime.

- Many workers are raiding their 401(k)s via loans or hardship withdrawals just to cover current expenses, undermining their future.

The math of retirement isn’t mysterious. But the combination of:

- Stagnant or inconsistent savings,

- Student loans and housing costs,

- Limited access to workplace retirement plans, and

- Behavioral mistakes during market volatility

creates a real retirement crisisespecially for people whose main “plan” is a house plus Social Security.

So What’s the Real “Biggest Problem in Finance”?

Putting it all together, the biggest problem in finance isn’t a single villain. It’s a three-part combo:

- Unequal ownership of productive financial assets (the wealthy own most of the stock market).

- Low, uneven financial literacy (many people never get basic money education).

- Human psychology (our biases push us toward short-term, emotional decisions).

When the people who understand and own financial assets also have the best tools, advice, and tax planning, their wealth compounds faster.

When everyone else is stuck in debt-heavy housing, living paycheck to paycheck, and trying to DIY their way through complex choices,

the gap naturally widens.

The good news? You don’t have to solve the global wealth gap to dramatically improve your own situation.

You just need a bit ofyescommon sense and a plan.

Practical Ways to Fight Back (Without Becoming a Finance Nerd)

1. Shift From “House-Only” to “House + Portfolio”

If your home is your biggest (or only) asset, make it a priority to gradually build a portfolio of low-cost, diversified funds.

Even small, regular contributions to an index fund or target-date retirement fund can change your long-term trajectory.

You don’t need to pick stocks. You don’t need to watch markets all day. You just need to:

- Contribute regularly (automate it if you can).

- Keep costs low.

- Stay invested through ups and downs.

2. Raise Your Savings RateGently but Relentlessly

Many financial planners suggest aiming to save around 15–20% of your gross income for long-term goals, including retirement.

That may not be realistic immediately, especially if you’re juggling high living costs, but you can:

- Start with 3–5% and increase 1–2 percentage points per year.

- Use raises and bonuses to boost contributions so your lifestyle doesn’t take a hit.

- Take full advantage of any employer match firstit’s effectively free money.

3. Build an Emergency Fund to Protect Your Future Self

One reason people raid their 401(k)s or rack up credit card debt is that they have no cushion. An emergency fund covering

3–6 months of essential expenses is boring but powerful.

Think of it as your “Do Not Panic” fund. It keeps you from turning short-term problems into long-term damage.

4. Hack Your Own Behavior

You can’t delete your biases, but you can design around them:

- Automate good decisions: automatic transfers to savings and investments.

- Pre-commit: decide in advance how you’ll respond to market crashes (e.g., “I won’t sell unless I lose my job and need cash”).

- Limit noise: constant financial news can trigger emotions; check your portfolio less often.

- Use simple rules: for example, own a global stock index fund, a bond fund, and cash, then rebalance once a year.

5. Level Up Your Literacy (Without Drowning in Jargon)

You don’t need a finance degree; you just need a core toolkit:

- Understand the basics of interest, inflation, compounding, and risk.

- Know how your retirement accounts work (401(k), IRA, etc.).

- Learn the difference between “good” debt (productive, low-rate) and “bad” debt (high-interest consumer debt).

A handful of well-chosen books, reputable online resources, and simple calculators can be more valuable than hours of social media “advice.”

Real-World Experiences: How This Plays Out in Everyday Life

To see how the biggest problem in finance shows up in practice, imagine three very common situations.

The High-Earner With Nothing to Show for It

Alex is in their mid-40s, earns a six-figure income, and owns a nice home with a sizable mortgage. On paper, things look great.

But there’s a catch: nearly all of their net worth is tied up in the house, with a modest 401(k) and very little cash savings.

When a health issue leads to a few months off work, Alex quickly burns through savings and starts leaning on credit cards.

The 401(k) suddenly looks like a tempting piggy bank. A hardship withdrawal solves the immediate problem but triggers taxes, penalties,

and years of lost compounding.

This is what happens when a household is “asset rich” in a house but “portfolio poor” in liquid, diversified investments and emergency savings.

The solution for someone like Alex is not necessarily to sell the houseit’s to gradually rebalance their financial life away from a

single, illiquid asset and toward a mix of savings and investments that can weather surprises.

The Late Starter Who Thinks It’s “Too Late”

Jordan is 52 and has just realized that retirement is no longer a distant concept. There’s some money in a 401(k), but not nearly enough.

The instinct is to panic and swing for the fences: chase high-risk stocks, options, or crypto in an attempt to “catch up.”

Financial planners routinely warn against this behavior, because it tends to end with buying at euphoric peaks and selling at fearful lows.

A more realistic (and common-sense) approach is:

- Increasing the savings rate as much as possible.

- Using catch-up contributions in retirement accounts.

- Sticking mostly to diversified funds rather than speculative bets.

- Exploring options like working a bit longer or part-time in retirement.

The math might not produce a “perfect” retirement number, but a steady, disciplined plan usually beats frantic gambling on the markets.

The Young Professional Who Actually Has an Edge

Finally, imagine Taylor, a 27-year-old who doesn’t make a huge salary yet but has two advantages many people overlook:

- Time.

- A willingness to learn.

By focusing on basicspaying off high-interest debt, building a small emergency fund, and contributing consistently to a low-cost

index fund inside a 401(k) or IRATaylor harnesses the one force even wealth inequality struggles to beat: compounding over decades.

Taylor doesn’t have to pick individual stocks or guess where the market will be next year. They just need to stay in the game,

increase contributions as income rises, and avoid the trap of lifestyle creep swallowing every raise.

When financial advisors and researchers talk about the “biggest problem in finance,” they’re not saying individuals are doomed.

They’re saying the system rewards those who:

- Get invested in productive assets early,

- Learn just enough to avoid major mistakes, and

- Design their lives around long-term goals instead of short-term impulses.

You can’t control who owns most of the global stock market. But you can control whether you’re an owner at all,

how consistently you save, and how you respond when markets get noisy. That’s where genuine “wealth of common sense” lives.

Conclusion: Common Sense as a Superpower

The biggest problem in finance isn’t some mysterious Wall Street algorithm or a secret rule you’ve never heard of.

It’s the gap between:

- Owning productive financial assets versus relying on a single home,

- Having basic money literacy versus winging it, and

- Thinking long-term versus reacting emotionally in the moment.

You don’t have to become obsessed with markets to improve your financial life. You just need a handful of simple habits:

save more over time, invest in low-cost diversified funds, protect yourself with an emergency fund, and learn enough to

recognize your own biases.

In a world obsessed with hot stock tips and financial “hacks,” the real edge is still what it has always been:

a little patience, a little humility, and a lot of common sense.

Citations for factual data: