Table of Contents >> Show >> Hide

- What a Hedge Actually Does

- The Most Common Hedges and Their Blind Spots

- Diversification: The First Defense, Not the Final One

- Bonds: Helpful, Until Inflation Crashes the Party

- TIPS: Better for Inflation, Not for Every Other Problem

- Gold and Commodities: Shiny, Famous, and Frequently Misunderstood

- Protective Puts and Collars: Real Protection, Real Price Tag

- Currency Hedges: Good for FX Risk, Not Business Risk

- Alternatives: Different Risks, Not Risk-Free Returns

- Why the Perfect Hedge Keeps Failing in the Real World

- How to Invest When No Hedge Covers Every Risk

- Experience: What This Looks Like in the Real World

- Conclusion

- SEO Tags

Every investor eventually goes looking for the same magical creature: the perfect hedge. It is usually imagined as a tidy little portfolio accessory that will rise when everything else falls, preserve purchasing power, calm nerves, lower taxes, keep liquidity handy, and still somehow leave upside wide open. In other words, a financial unicorn wearing a sensible blazer.

Here is the less glamorous truth: there is no hedge for everything. A hedge can protect against a specific risk, over a specific time frame, with a specific cost. That is useful. It is also limited. A bond hedge may struggle during an inflation shock. Gold may shine brilliantly for a while and then behave like an unreliable weather app. Protective puts can cushion losses, but they are not free. Currency hedges can reduce foreign exchange swings, but they cannot rescue a bad business or a weak market. Even diversification, the most sensible tool in the kit, is not a force field.

That does not mean hedging is pointless. Far from it. It means smart investors stop asking, “What protects me from everything?” and start asking better questions: “What am I really exposed to?” “What damage would matter most?” “How much protection do I need?” and “What am I willing to pay for it?” That shift in thinking is the difference between risk management and wishful thinking dressed up as strategy.

What a Hedge Actually Does

A hedge is not a cure-all. It is a trade-off. At its core, hedging means reducing one risk by taking on another cost, constraint, or offsetting exposure. Sometimes that cost is obvious, such as an options premium. Sometimes it is hidden in lower returns, tax complexity, lost upside, liquidity limits, or the simple discomfort of holding something boring while fashionable assets strut around the market like peacocks.

That is why the phrase There is No Hedge For Everything matters so much. Risk is not one giant blob. It comes in flavors. There is market risk, inflation risk, interest-rate risk, credit risk, currency risk, liquidity risk, concentration risk, and timing risk. A tool that helps with one of them may do very little for the others. Some hedges can even create new headaches while solving the first one.

Think of it like homeownership. A fire extinguisher is excellent if your toaster stages a rebellion. It is less useful against termites, flooding, or a roof that decides gravity is optional. Financial hedges work the same way. Useful? Absolutely. Universal? Not even close.

The Most Common Hedges and Their Blind Spots

Diversification: The First Defense, Not the Final One

Diversification deserves respect because it remains one of the most practical ways to reduce portfolio risk. Spreading money across asset classes, industries, geographies, and security types can lower the odds that one bad bet becomes a full-blown catastrophe. It can smooth the ride. It can reduce concentration. It can help investors stay invested instead of panic-selling at exactly the wrong moment.

But diversification is not a magic spell. When broad markets fall together, diversified portfolios can still lose money. They may lose less than concentrated portfolios, which is not nothing, but “less terrible” and “fully protected” are very different outcomes. That distinction matters. Plenty of investors say they want downside protection, but what they really built was a better-shaped version of the same storm.

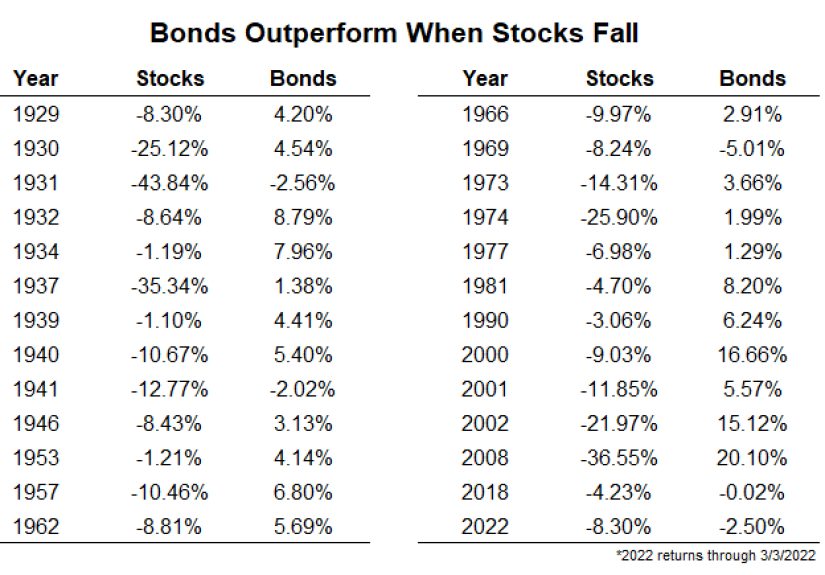

Bonds: Helpful, Until Inflation Crashes the Party

For years, many investors treated high-quality bonds as the dependable adult in the room. Stocks were invited to dance on the table. Bonds were asked to keep the furniture from breaking. That relationship often worked because bonds tended to cushion equity downturns, especially during growth scares or recessions.

But the stock-bond relationship is not fixed in stone. In higher-inflation environments, stocks and bonds can fall together. That ugly possibility became painfully memorable in 2022, when rising inflation and aggressive rate increases hit both sides of the traditional 60/40 portfolio. The lesson was not that bonds are useless. The lesson was that bonds are not a hedge against every kind of bad day. They are particularly vulnerable when the problem is inflation and rising yields rather than weak growth alone.

TIPS: Better for Inflation, Not for Every Other Problem

Treasury Inflation-Protected Securities, or TIPS, are one of the clearest examples of targeted protection. They are designed to help investors defend against inflation because their principal adjusts with changes in the Consumer Price Index. That makes them much more direct as an inflation hedge than simply hoping ordinary bonds will somehow tough it out.

Still, TIPS do not protect against every risk that matters. Their market prices can fluctuate. Real yields matter. Timing matters. If you buy them at the wrong point or sell before maturity, the experience may be bumpier than the label “inflation protection” suggests. TIPS are useful tools for inflation risk. They are not a master key for equity crashes, credit events, or liquidity needs.

Gold and Commodities: Shiny, Famous, and Frequently Misunderstood

Gold has one of the best marketing teams in investing, and the marketing team is history. It is famous for preserving purchasing power over long stretches, and it often gets attention during inflation scares, geopolitical stress, or periods of mistrust in paper assets. Commodities more broadly can also help during inflation surprises because raw materials tend to sit closer to the source of rising prices.

That said, investors often oversimplify the story. Gold is not a guaranteed short-term inflation hedge. Its performance can disappoint, especially when real interest rates rise. Commodities can be useful, but they are volatile, cyclical, and far from cuddly. They can diversify a portfolio, yet they can also whipsaw investors who expected a smooth insurance product and got a roller coaster with no cup holders.

In other words, gold may hedge some fears, commodities may hedge some inflation shocks, and neither one promises emotional comfort on demand.

Protective Puts and Collars: Real Protection, Real Price Tag

Options are one of the few places where downside protection can be defined with impressive precision. A protective put can place a floor under losses for a period of time. A collar can reduce the cost of that protection by giving up some upside. These are serious tools, not market folklore.

But precision comes with a bill. Put premiums can be expensive, especially when volatility is already high and everyone suddenly wants insurance at the same time. Buy protection too often, and the repeated cost can drag on returns. Use a collar, and the reduced cost usually comes with capped gains. Hedge only part of a portfolio, and the protection is incomplete. Hedge with the wrong benchmark, and the fit may be sloppy. Options can work very well, but they do not repeal the laws of cost, timing, and trade-offs.

Currency Hedges: Good for FX Risk, Not Business Risk

International investing adds another layer of complexity because returns are influenced not just by the underlying investment, but also by exchange rates. A strong foreign asset can look weaker once translated back into dollars, and the reverse can also happen. Currency hedging can reduce that volatility, which is why it is often more compelling for international bonds than for international stocks.

Still, currency hedging is not perfect. It aims to reduce exchange-rate risk, not eliminate all uncertainty. It can mute gains from favorable currency moves. It may be less effective than investors expect. And it certainly does not protect against poor fundamentals, geopolitical trouble, or bad security selection. It is a seatbelt for one kind of impact, not a miracle suspension system for the whole road.

Alternatives: Different Risks, Not Risk-Free Returns

When traditional portfolios stop feeling safe, investors often wander into the land of alternatives. Private credit, hedge funds, managed futures, real assets, structured products, and other “uncorrelated” strategies can sound like the answer to everything. Sometimes they do offer meaningful diversification benefits. Some can be especially helpful in specific market regimes.

But alternatives are not fairy dust. They can carry high fees, limited liquidity, complexity, leverage, valuation opacity, and long lockups. A strategy with low correlation is not the same as a strategy with low risk. Some alternatives diversify beautifully until investors need cash, at which point the fine print arrives wearing boots.

Why the Perfect Hedge Keeps Failing in the Real World

The reason there is no hedge for everything is simple: markets do not break in one consistent way. Sometimes the threat is recession. Sometimes it is inflation. Sometimes it is a credit squeeze, policy shock, war scare, or a rush for liquidity. Sometimes the hedge itself becomes crowded and expensive. Sometimes the hedge works, but the investor sized it badly. Sometimes it works too late. Sometimes it works, but not against the particular thing that actually went wrong.

This is why portfolio construction matters more than clever slogans. The goal is not to own a single superhero asset. The goal is to build a system where different pieces help under different conditions, while acknowledging that no single piece will do all the heavy lifting. That is less romantic than searching for the one hedge to rule them all, but it is a lot more useful.

How to Invest When No Hedge Covers Every Risk

1. Identify the risk before buying the solution

If you are worried about inflation, say inflation. If you are worried about a stock-market crash, say that. If you are worried about needing cash next year, that is a liquidity problem, not a diversification problem. Investors get into trouble when they buy a product because it sounds defensive without matching it to the risk they actually face.

2. Match the horizon to the hedge

Protection is time-sensitive. Short-dated options can expire before the trouble arrives. Long-duration bonds can help in one regime and hurt in another. A hedge that works beautifully over a decade may be miserable over six months. Time horizon is not a footnote. It is part of the trade itself.

3. Accept that good hedges usually cost something

If the protection looks free, look again. Maybe the cost is hidden in fees, taxes, complexity, illiquidity, lower expected returns, or capped upside. The market is many things, but it is rarely in the business of giving away attractive insurance with no strings attached.

4. Build layers, not fantasies

A resilient portfolio usually relies on several partial defenses instead of one dramatic bet. Cash can help with liquidity. Bonds can still help with stability in many scenarios. TIPS can address inflation more directly. Selective diversification can reduce concentration. Options may be useful for temporary risk control. None is perfect. Together, they can be practical.

5. Remember behavior is part of risk management

The best hedge on paper is useless if it is so complicated, expensive, or uncomfortable that you abandon it halfway through a crisis. A simpler, imperfect strategy that you can actually stick with often beats an elegant masterpiece that falls apart the moment the headlines start screaming in all caps.

Experience: What This Looks Like in the Real World

Investors rarely learn the lesson “there is no hedge for everything” in a quiet, philosophical way. Usually, the market teaches it with a frying pan. One person buys gold expecting it to save the day, only to discover that gold can have long stretches of looking moody, expensive, and not particularly interested in rescuing anyone by Friday afternoon. Another loads up on long bonds for safety, then watches inflation and rising rates turn the “safe” part into an uncomfortable conversation. A third investor buys protective puts only after volatility has already jumped, paying luxury pricing for basic insurance and then feeling cheated when the market calms down before the hedge pays off.

A retiree might think dividend stocks are a hedge because they feel sturdier than flashy growth names. Sometimes they are. But dividends do not stop prices from falling in a panic, and companies can cut payouts when business conditions get rough. A business owner may keep too little cash because cash feels unproductive, then discover that liquidity is not boring at all when payroll is due and credit suddenly tightens. An internationally diversified investor may celebrate foreign exposure during a weak-dollar stretch, only to feel blindsided when currency movements reverse and eat into returns. None of these people made irrational choices. They just treated one useful tool as if it solved every problem in the house.

Real experience also shows something encouraging: investors do not need perfection to do better. The ones who weather difficult markets tend to be the ones who stop demanding that every portfolio sleeve behave like a hero. They let stocks do the long-term growth work. They let cash handle near-term needs. They use bonds for stability with open eyes about inflation risk. They use TIPS when inflation matters. They may use options tactically instead of permanently. They understand that unhedged international equities can add diversification, while hedged international bonds may better preserve the bond role in a portfolio. Most of all, they expect disappointment somewhere. That expectation, oddly enough, makes them more resilient.

The market has a dark sense of humor. The protection everyone wants is usually most expensive when fear is already high. The assets that looked safest last year may be the ones under pressure this year. The old correlation map gets redrawn. The “sure thing” becomes a very educational mistake. That is why durable investing is less about finding a flawless hedge and more about building a portfolio that can survive being occasionally wrong.

So yes, there is no hedge for everything. That sounds discouraging until you realize what it actually means. You do not need omnipotence. You need clarity. You need to understand which risks matter most to your goals, which tools address those risks, what each tool costs, and what it leaves behind. Once you accept that every hedge is partial, your decisions often get smarter, calmer, and less theatrical. And in investing, less theatrical is usually a very profitable personality trait.

Conclusion

The search for the perfect hedge is understandable, but it leads many investors in the wrong direction. A better approach is to stop chasing universal protection and start building intentional protection. Diversification helps, but it cannot eliminate losses. Bonds can stabilize a portfolio, but they are not invincible during inflation shocks. TIPS can target inflation, options can define downside for a price, currency hedging can reduce foreign-exchange noise, and alternatives may diversify certain exposures, but every one of these tools comes with limitations.

That is the real lesson behind There Is No Hedge For Everything: successful risk management is not about owning one flawless defensive asset. It is about understanding that different risks require different responses, and no response is free. Investors who accept that trade-off tend to build portfolios that are more durable, more realistic, and far less dependent on market myths. In a world where uncertainty never fully clocks out, that mindset may be the closest thing to a genuine edge.