Table of Contents >> Show >> Hide

- What “Totaled” Actually Means (And What It Doesn’t)

- The Two Main Rules Insurers Use: Threshold vs. Formula

- The Numbers That Decide Your Fate

- It’s Not Only Math: Safety and Practical Repairability

- Concrete Examples: When a Car Is Considered Totaled

- What Happens After Your Car Is Declared a Total Loss?

- Can You Keep a Totaled Car? (Yes, But Read This Twice)

- How to Negotiate a Total-Loss Settlement (Without Becoming a Villain)

- Totaled vs. Salvage vs. Rebuilt: Quick Definitions

- FAQs People Google at 1:12 a.m.

- Key Takeaways (So You Can Stop Doom-Scrolling)

- Extra: Real-World “Totaled” Experiences (Lessons From the Claims Trenches)

Your car can be declared “totaled” even if it still starts, still drives, and still has that one floor mat you’ve been meaning to vacuum since 2019.

Annoying? Yes. A conspiracy? Usually no. It’s mostly math, state rules, and a dash of “we found more damage once we took the bumper off.”

In standard U.S. insurance terms, a car is considered totaled (a total loss) when repairing it no longer makes economic sense

or when it can’t be restored to safe, pre-crash condition at a reasonable cost. Below is the real-world breakdown: how insurers decide, what numbers matter,

and what you can do if you don’t love the decision (or the settlement offer).

What “Totaled” Actually Means (And What It Doesn’t)

A vehicle is “totaled” when your insurance company determines it’s a total loss. That usually means:

the cost to repair the vehicle (sometimes plus additional costs like salvage value) meets or exceeds the vehicle’s

actual cash value (ACV)what it was worth right before the loss.

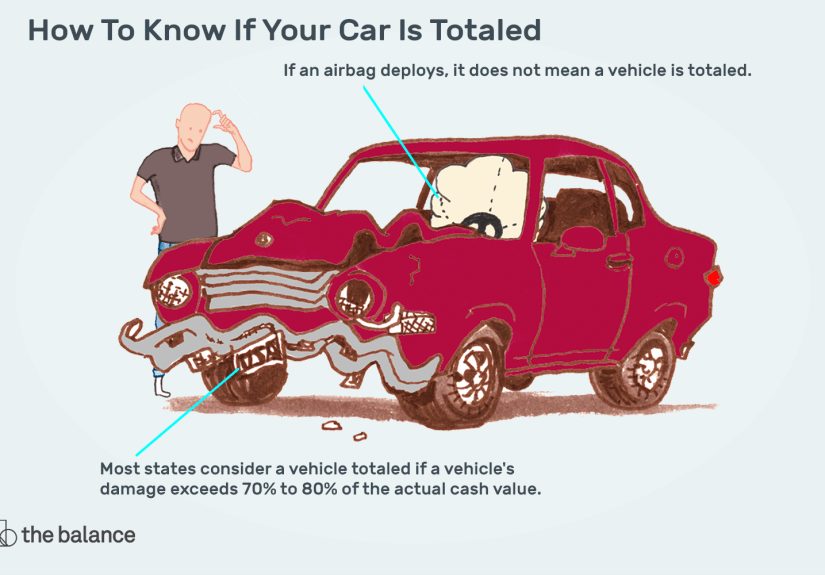

Important: “Totaled” does not mean “turned into a flaming pile of regret.” It can mean the damage is moderate but expensiveespecially on

newer vehicles with sensors, cameras, airbags, specialty materials, and parts that are priced like they’re handcrafted by polite Swiss engineers.

The Two Main Rules Insurers Use: Threshold vs. Formula

1) Total Loss Threshold (TLT): a percentage trigger

Many states use a total loss threshold: if repair costs reach a certain percentage of the car’s value, the vehicle is considered totaled.

Thresholds vary by state and can be surprisingly different. Also, insurers may choose to total a car even below the threshold if it’s still not

economically or safely repairable.

2) Total Loss Formula (TLF): the “repairs + salvage” test

Other states use a total loss formula, commonly expressed like this:

(Repair Cost + Salvage Value) ≥ Actual Cash Value.

Translation: if fixing the car plus what the damaged car could sell for at salvage meets or exceeds what the car was worth pre-loss, it’s a total loss.

(This approach is often called a constructive total loss method.)

The Numbers That Decide Your Fate

Actual Cash Value (ACV): what your car was worth yesterday

ACV is basically the car’s pre-loss market value, considering year, make/model, trim, mileage, condition, prior damage, options, and

local market data. It’s closer to “what you could have sold it for last week” than “what you still owe” or “what it costs brand-new.”

Insurers often rely on vehicle valuation databases and comparable sales/listings, then adjust based on your specific vehicle details. This is why small

errorswrong trim, missing options, incorrect mileage, or “condition” marked too lowcan move your settlement.

Repair cost estimate: the visible damage plus the surprise damage

The initial repair estimate is built from parts and labor needed to restore the vehicle to pre-loss condition. But modern repairs can balloon quickly:

ADAS recalibration, airbag modules, wiring harnesses, specialty paint, aluminum repair procedures, and “oh look, the radiator support is also toast.”

And yes, insurers know supplements happen. A car that looks “mostly fine” can become a total loss once a shop discovers hidden structural or mechanical damage.

Salvage value: what your damaged car is worth to someone else

Even badly damaged vehicles have valueparts, scrap metal, and rebuild potential. That value is the salvage value. When states use the

total loss formula, salvage value can be the deciding factor that pushes a borderline repair into “totaled” territory.

It’s Not Only Math: Safety and Practical Repairability

Insurance companies can also total a vehicle because it’s not reasonably repairable to a safe standardeven if the raw math looks close.

Common “safety/feasibility” reasons include:

- Structural damage (frame/unibody areas) that can’t be restored reliably.

- Airbag deployment paired with extensive interior and sensor replacement.

- Flood damage, where corrosion and electrical problems can be long-term nightmares.

- Fire damage, where heat can compromise materials and wiring in unpredictable ways.

- Parts availability delays or manufacturer repair procedures that sharply increase labor hours.

The uncomfortable truth: some cars can be repaired, but the “after” version may be less safe, less reliable, harder to insure, and worth much less.

Totaling is often the insurer’s way of avoiding a risky repair outcome.

Concrete Examples: When a Car Is Considered Totaled

Example A: The older car with “too much” repair cost

Your 2014 sedan has an ACV of $7,500. A body shop estimates $6,200 in repairs after a rear-end crash (bumper, trunk, quarter panel, sensors).

In a state with a 75% threshold, $6,200 is about 83% of $7,500so it’s likely a total loss. Even if the car seems drivable, the repair cost-to-value ratio

is the deal-breaker.

Example B: The formula state where salvage tips it over

ACV is $10,000. Repairs are $7,400. Salvage value is $3,000. Using the formula:

$7,400 + $3,000 = $10,400, which is ≥ $10,000. Result: totaled.

This is why people sometimes hear “But repairs are less than the value!” and still get a total loss decision.

Example C: Newer car, “small” crash, big-tech bill

A minor-looking front-end hit on a newer vehicle triggers: bumper cover, radar sensor, grille shutters, headlight assembly, calibration, plus labor.

The parts alone can climb into the thousands. Add shop labor rates and calibration, and you can hit total-loss territory faster than your brain expects.

Example D: Flood damage, where the insurer says “nope”

Water intrusion can mean electrical issues that pop up months later. Even if the car starts today, corrosion and module failures can become a slow-drip

expense faucet. Many insurers total flood-damaged vehicles because “repaired” doesn’t reliably mean “safe and predictable.”

What Happens After Your Car Is Declared a Total Loss?

A total-loss claim usually follows this flow:

- Inspection & estimate (adjuster and/or repair shop).

- Valuation to determine ACV using local market data and vehicle details.

- Total loss determination using your state’s rule and insurer guidelines.

- Settlement offer (ACV, minus deductible if applicable, plus/including certain taxes/fees depending on state/practice).

- Title handling (insurer takes ownership, or you retain salvage).

- Payout to you and/or your lender/lessor.

If you own the car outright

Typically, you receive a payout based on ACV (minus your deductible if you’re claiming under your own policy). The insurer then takes the vehicle and sells

it through salvage channelsunless you choose to keep it (more on that soon).

If you have a loan or lease

The settlement usually goes to the lender first, because the lender has a financial interest in the car. If the payout exceeds the loan balance, you get the

remainder. If it’s less, you may owe the gapunless you have gap insurance, which can cover the difference between the ACV payout and the

remaining loan/lease balance.

Watch the clock: storage fees and rental coverage

Tow yards and storage facilities can charge daily fees, and rental coverage may have limits. In many claims, delays cost moneyso respond quickly, document

everything, and ask the adjuster what deadlines apply to moving the vehicle, accepting the settlement, or retaining salvage.

Can You Keep a Totaled Car? (Yes, But Read This Twice)

In many situations, you can keep the vehicle after it’s totaledoften called owner retention. Usually the insurer reduces your payout by

the vehicle’s salvage value, since they’re not taking the car to sell it.

Here’s the catch: keeping a totaled car typically triggers a salvage title (or a similar brand) through your state DMV. To drive it again,

you may need repairs, inspections, and a rebuilt or rebuilt salvage title. Requirements vary by state, and insurance

availability can be limited until the title status is sorted out.

When keeping it can make sense

- Damage is largely cosmetic, and you’re confident it’s safe after repair.

- You can do some repairs yourself (properly) or have a trusted shop at a lower cost.

- The vehicle is rare, sentimental, or already “not worth much” but still useful to you.

- You want it for parts (especially if it has upgrades you can reuse).

When keeping it is usually a bad idea

- Flood damage (electrical and corrosion issues can haunt you).

- Major structural damage or questionable repairs.

- You need full coverage insurance easily and cheaply (salvage/rebuilt can complicate this).

- You plan to resell soon (branded titles often slash resale value).

How to Negotiate a Total-Loss Settlement (Without Becoming a Villain)

If you think the ACV is too low, you’re not powerless. The goal is not to “win a debate,” but to correct the data and prove the market.

Here’s a practical, non-drama checklist:

1) Ask for the valuation report

Request the detailed valuation showing comparable vehicles and adjustments. Look for mistakes: trim level, drivetrain, packages, mileage, condition, options,

prior accident history, even your ZIP code.

2) Bring your own comparable listings

Find listings for similar year/make/model/trim with similar mileage in your area (or the nearest reasonable market). Don’t cherry-pick unicorn prices;

use realistic comps and explain why they match.

3) Document condition and upgrades

Recent tires, major maintenance, battery, brakesthese can support a higher condition rating. Provide receipts and photos. You won’t get dollar-for-dollar

reimbursement for upgrades, but you can often justify a better condition adjustment.

4) Confirm what’s included in the offer

Depending on state rules and insurer practice, the settlement may include taxes and certain fees. Ask what’s included and what isn’t, so you’re comparing

apples to apples.

5) Use the policy options if you hit a wall

Some policies include an appraisal/independent valuation process for disputes. If you feel truly stuck, you can also contact your state’s insurance

department for consumer guidance. (Save that step for after you’ve calmly presented your evidencebeing organized gets better results than being loud.)

Totaled vs. Salvage vs. Rebuilt: Quick Definitions

- Total loss / totaled: insurer decides it’s not economically or safely repairable under the applicable rule.

- Salvage title: the state brands the title to show the vehicle was declared a total loss.

- Rebuilt title: the salvage vehicle was repaired and passed required inspections (rules vary by state).

- Diminished value: loss in market value because the vehicle now has an accident historyeven after repairs (availability and rules vary).

FAQs People Google at 1:12 a.m.

My car is totaled but still drivable. Can I keep driving it?

Sometimes, temporarilydepending on damage, legality, and whether it’s been issued a salvage brand or deemed unsafe. But if the car is structurally unsafe,

has compromised airbags, or has significant mechanical issues, driving it is risky. Also, once a vehicle is branded salvage, states may restrict registration

until inspection/rebuild steps are completed.

Does a total loss hurt my credit?

The total loss itself doesn’t “hit” your credit like a missed payment would. Credit issues usually happen only if the loan isn’t paid off (or if you miss

payments while the claim is being resolved). If you owe more than the ACV, gap insurance can be the difference between “annoying day” and “financial migraine.”

What if the body shop says it can be fixed?

A car can be physically repairable but still not make economic sense to fix. Insurers decide based on cost, rules, and risk. You can challenge the valuation

or keep the car (if allowed), but don’t confuse “possible” with “practical.”

What if the other driver is at fault?

You may pursue the claim through the at-fault driver’s insurance (property damage liability), or through your own collision coverage (then your insurer may

seek reimbursement). The total loss decision process is similar: value the car, estimate repairs, apply the rule.

Key Takeaways (So You Can Stop Doom-Scrolling)

- A car is considered totaled when repair costs (sometimes plus salvage value) meet/exceed ACV under your state’s rule or insurer guidelines.

- States typically use either a percentage threshold or a total loss formula; insurers may total a car even below the threshold in some cases.

- ACV is market value pre-lossnot your loan balance and not replacement cost new.

- You can often negotiate the settlement by correcting vehicle details and providing solid comparable listings.

- Keeping the car is possible, but salvage/rebuilt title rules and insurance availability can be a headachesometimes a manageable one, sometimes not.

Bottom line: the total-loss decision is usually the insurer choosing the least-worst financial path. Your job is to make sure the numbers are accurate,

the process is fair, and your next step matches your real life (budget, safety, time, and tolerance for paperwork).

Extra: Real-World “Totaled” Experiences (Lessons From the Claims Trenches)

The weirdest part of learning when a car is considered totaled is realizing how often it doesn’t match what your eyes are telling you. One of the

most common stories goes like this: “The car drives fine, the trunk even closes, and yet the adjuster said it’s a total loss.” That usually happens because

the damage is concentrated in expensive areasrear quarter panels, crumple zones, sensor-packed bumpers, or anything that requires hours of labor plus parts

that arrive in a box labeled “mortgage payment.” A drivable car can still be a terrible financial repair.

Another frequent scenario: the “small hit, big bill” modern-car surprise. Drivers expect a scratch and a quick repaint. Then the estimate includes a radar

unit, a camera bracket, calibration procedures, and specialty fasteners the manufacturer insists must be replaced (not reused). Suddenly, a low-speed

impact is priced like a high-speed regret. It’s not that shops are making it upit’s that cars have become rolling computers with safety systems that must be

returned to precise factory specs.

Flood events create their own brand of heartbreak. People often assume: “If it dries out, it’s fine.” But claim outcomes tend to be harsher because water

doesn’t just wet carpetsit can creep into connectors, modules, and harnesses. Months later, the car may develop electrical gremlins that turn routine driving

into a game of “Which warning light is the new one?” Insurers tend to be conservative here because unpredictable failures aren’t just inconvenientthey can be

dangerous.

There’s also the negotiation experienceless dramatic than movies, but still important. Many drivers improve a total-loss offer simply by spotting a wrong trim

level, missing options (sunroof, premium audio, safety package), or an unfair condition grade. The best approach is calm and evidence-based: ask for the

valuation details, provide comparable local listings, and include maintenance receipts that support the car’s pre-loss condition. It’s not about “arguing”

so much as “auditing.”

Finally, some owners choose to keep a totaled carand sometimes it’s a smart move. A classic example is cosmetic damage on an older vehicle that has already

lived a full, meaningful life of grocery runs and questionable drive-thru decisions. If the core structure is sound and a trusted shop can repair it safely,

retaining salvage can keep a reliable car on the road for less than replacing it in today’s market. But the people who do best with this route treat it like

a project with paperwork: they budget for inspections, understand title branding rules, and accept that resale value will take a hit. In other words, they

go in with eyes openboth eyes, ideally, not the “I’ll figure it out later” squint.

If there’s one universal lesson from these real-world situations, it’s this: totaled isn’t an insult to your car’s character. It’s a financial and regulatory

decision. Your best outcome comes from understanding the math, the state rule, and your own prioritiesthen choosing the path that makes your future self say,

“Okay, that wasn’t fun, but at least it was handled right.”