Table of Contents >> Show >> Hide

- What “Mean Reversion” Actually Means (And What It Doesn’t)

- The Most Annoying Truth: Mean Reversion Has No Deadline

- History’s Message: Even “Great” Runs Include Plenty of Pain

- Why Mean Reversion Feels “Broken” in Modern Markets

- So… When Is the Mean Reversion Coming?

- What the Pros Actually Do With Mean Reversion: They Use It for Expectations, Not Predictions

- Investor Playbook: How to Prepare Without Pretending You Have a Crystal Ball

- What Mean Reversion Could Look Like From Here: Four сценарии (No, You Don’t Have to Pick One)

- Bottom Line: The Smart Bet Is Not on TimingIt’s on Behavior

- Real-World Investor Experiences (500+ Words): What Mean Reversion Feels Like Up Close

If you’ve been investing for more than five minutes, you’ve heard the phrase mean reversion.

It’s the market’s version of “what goes up must come down,” except the market is a drama queen and

never tells you when, how, or how loudly.

The question gets especially popular after long stretches of strong returnswhen headlines start sounding

like the stock market has been guzzling espresso shots and bench-pressing record highs.

Investors look at eye-popping performance and wonder: “Okay… so when does the hangover hit?”

Here’s the twist: mean reversion is real, but it’s not a train schedule. You can’t set your watch to it.

And the market has a long history of making “obvious” outcomes painfully late, weirdly shaped,

and emotionally inconvenient.

What “Mean Reversion” Actually Means (And What It Doesn’t)

Mean reversion is the tendency for extreme outcomes to drift back toward more normal levels over time.

In markets, people usually mean one (or more) of these:

- Returns mean reversion: after unusually strong years, future returns are often lower (and vice versa).

- Valuation mean reversion: expensive markets (high P/E, high CAPE) tend to deliver lower long-run returns.

- Leadership mean reversion: yesterday’s winners eventually stop winning as much.

- Volatility mean reversion: calm periods tend to be followed by choppier ones.

What mean reversion doesn’t guarantee is a dramatic crash on a convenient date.

It can show up as a correction, sure. But it can also appear as a long stretch of “nothing happens”

while earnings catch up, valuations cool off, and investors slowly lose the ability to brag at parties.

The Most Annoying Truth: Mean Reversion Has No Deadline

Investors love clean stories: “Valuations are high, therefore the market must fall soon.”

But markets don’t operate like a math textbook. They operate like a crowd, and crowds have moods.

A big reason people get whiplash is that there are multiple paths to mean reversion:

Path 1: The Classic Drop

Prices fall faster than fundamentals. Valuations compress. Everyone suddenly becomes a “risk manager.”

This is the version that gets all the attention because it’s loud and cinematic.

Path 2: The Sideways Grind

The market goes nowhere for years while earnings and cash flows rise. Valuations cool off without a giant crash.

This is the version nobody posts about because “I earned 0% for 36 months” is not viral content.

Path 3: The Rotation

The index doesn’t necessarily collapse, but leadership changes. A narrow group stops carrying the team,

while other areas (value, small caps, international stocks, dividend payers) start contributing more.

The frustrating part is that all three paths can feel like mean reversion isn’t happeninguntil you zoom out.

Markets are excellent at confusing people in the short run and humbling them in the long run.

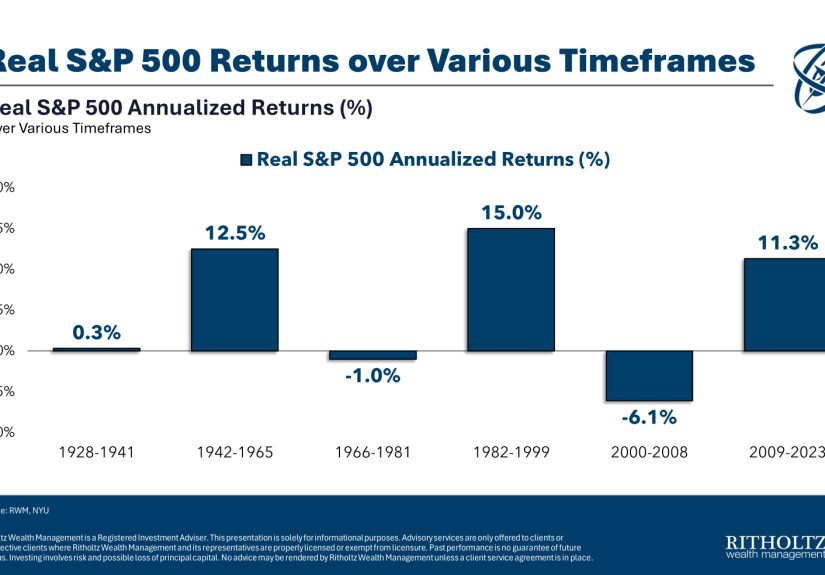

History’s Message: Even “Great” Runs Include Plenty of Pain

One reason mean reversion talk spikes during strong markets is that people forget how messy bull markets are.

A long-term uptrend doesn’t look like a smooth escalator. It looks like a hiking trail:

progress, setbacks, wrong turns, and the occasional “why am I doing this?” moment.

Consider a few historical reminders:

-

Big uptrends still contain frequent corrections. It’s normal to see multiple double-digit pullbacks

even during powerful multi-year runs. -

“Bad decades” can contain huge rallies. Inflationary eras, recessions, and ugly headlines can still produce

strong multi-year bursts inside the chaos. -

It’s hard to identify regimes in real time. Investors usually label periods “secular bull” or “secular bear”

after the factright around the time it becomes useless as a trading signal.

This is why the “mean reversion is coming” crowd often sounds right for a long time… until timing matters.

Being early in markets can look exactly like being wrong.

Why Mean Reversion Feels “Broken” in Modern Markets

If mean reversion is so powerful, why can markets stay expensive for so long? A few reasons show up again and again:

1) The Market’s “Mean” Can Move

The stock market isn’t a laboratory experiment with fixed conditions. The economy evolves.

Accounting changes. Index composition changes. Profit models change.

When the underlying engine changes, the historical average you’re reverting to might not be the same average you remember.

2) Valuations Can Be a Terrible Short-Term Timer

Valuation metrics (like CAPE, forward P/E, price-to-fair-value) are often more useful for

setting long-term expectations than for predicting next quarter’s returns.

Expensive markets can keep getting more expensiveespecially when enthusiasm meets a compelling narrative.

3) Concentration Can Delay the “Reversion” Feeling

When a small group of mega-companies dominates index performance, the overall market can look unstoppable

even if many stocks are just kind of… existing.

Narrow leadership can persist longer than bears expect, then reverse faster than bulls imagine.

4) Liquidity, Rates, and Psychology Matter

Investor willingness to pay up for future growth shifts with interest rates, inflation expectations,

economic confidence, and plain old FOMO.

Sometimes the market isn’t “ignoring” mean reversionit’s debating what the right price of risk should be.

So… When Is the Mean Reversion Coming?

The most honest answer is: it’s always coming, and it’s always here, just not evenly distributed.

Some areas are reverting while others are extending. Some investors experience mean reversion as a crash.

Others experience it as a decade of “fine, I guess” returns.

A more practical answer is to stop treating mean reversion like a prophecy and start using it like a

planning tool. The goal isn’t to guess the exact month the market “gets normal.”

The goal is to build a portfolio that can survive the process.

What the Pros Actually Do With Mean Reversion: They Use It for Expectations, Not Predictions

Many serious market outlooks today share a similar theme:

long-term returns for U.S. stocks may be more muted than what investors have grown used to.

That doesn’t mean a crash is scheduled. It means future returns could be lower because starting valuations are higher.

Think of it this way: if you start a road trip already halfway to your destination,

you don’t have as much road left to travel. High starting prices can reduce the “room” for future gains,

unless fundamentals grow fast enough to justify them.

A quick “math without pain” example

Suppose the market has compounded at a very high rate for a long stretch. Mean reversion can happen if:

- you get one ugly year (a big drawdown), or

- you get many quiet years (low single-digit returns), or

- you get a mix (a couple of down years plus a longer stretch of meh).

Notice how only one of those requires a dramatic collapse. The market can revert by boring you to death.

It’s not personal. It’s just rude.

Investor Playbook: How to Prepare Without Pretending You Have a Crystal Ball

1) Diversify like you actually mean it

Diversification isn’t a trendy sloganit’s a recognition that leadership changes.

If your portfolio is basically “the same trade in different fonts,” mean reversion will eventually introduce you to regret.

2) Rebalance with discipline, not drama

Rebalancing is one of the few investor behaviors that quietly forces “sell a little of what’s expensive, buy a little of what’s cheaper.”

You can do it on a schedule (once a year), by thresholds (when allocations drift meaningfully), or a hybrid approach.

3) Separate “market risk” from “life risk”

If you might need the money soon, the stock market is the wrong place for it.

The most painful mean reversion experiences usually happen when investors are forced to sell during downturns.

An emergency fund isn’t a return generatorit’s a decision generator.

4) Don’t confuse “lower expected returns” with “no returns”

A decade of lower returns can still be positive.

It might just look unimpressive compared to a red-hot decade.

That’s not the market failing. That’s the market returning to something closer to normal.

5) Keep your process simple enough to follow in a bad month

The best plan is the one you can execute when the market is down, your group chat is panicking,

and your brain is trying to convince you that this time is definitely different (again).

What Mean Reversion Could Look Like From Here: Four сценарии (No, You Don’t Have to Pick One)

Scenario A: The Fast Flush

A sharp correction or bear market knocks valuations down quickly. It feels terrible in real time,

but it resets expected returns faster. This is the “ripping off the Band-Aid” version.

Scenario B: The Long Plateau

Stocks churn sideways while earnings grow. Investors get restless, then bored, then impatient,

then tempted by whatever is currently trending. This scenario “reverts” expectations without a crash.

Scenario C: The Quiet Rotation

The overall index remains okay, but the leadership baton gets passed.

The experience for investors depends heavily on whether they own only the former leaders or a broader mix.

Scenario D: The Fundamental Catch-Up

Strong earnings growth supports high prices. Valuations might ease, but not collapse.

The market “earns” its way out of being expensive. This is the least painful scenario,

and therefore the one everyone wants… which is exactly why it won’t always happen.

Bottom Line: The Smart Bet Is Not on TimingIt’s on Behavior

Mean reversion is not a villain hiding behind the curtain waiting to jump out on a Tuesday.

It’s a long-run tendency that shows up in different ways, at different speeds, and often in the most annoying form possible.

If you build your entire strategy around predicting the exact moment the market “goes back to normal,”

you’re making a high-confidence bet in a low-certainty environment.

A better approach is to accept that cycles exist, prepare for them, and keep your financial life sturdy enough

that you don’t have to make desperate decisions when the market gets moody.

Because mean reversion is coming. The only mystery is whether it arrives like a thunderstorm,

a slow leak, or a surprise plot twist in the third season.

Real-World Investor Experiences (500+ Words): What Mean Reversion Feels Like Up Close

Most investors don’t experience mean reversion as a neat chart in a research report.

They experience it as a series of very human moments: hesitation, overconfidence, second-guessing,

and the occasional midnight scroll through market commentary that somehow makes everything feel worse.

Here are a few common “investor stories” that show how mean reversion tends to play out in real life.

The “All-Time-High Skeptic”

This investor sees the market hit new highs and treats it like a horror movie character walking into a dark basement:

“Don’t do it!” They wait for the “inevitable” pullback, holding cash because buying now feels reckless.

Sometimes they get a correction and feel vindicated… right up until the market rebounds before they actually buy.

Their mean reversion experience isn’t a crashit’s the slow realization that being cautious can still be costly

when caution turns into chronic hesitation.

The “Mean-Reversion Timer”

This investor builds an identity around calling the top. They collect valuation charts the way other people collect memes.

They’re not always wrong on direction; they’re wrong on time. Meanwhile, the market keeps rising,

and their portfolio underperforms. Eventually they either capitulate near a peak (classic),

or they stay stubborn through an entire cycle (also classic).

Their key lesson is brutal but useful: a correct thesis with bad timing can still produce bad results.

The “Rebalancer Who Sleeps Better”

This investor doesn’t try to predict the moment mean reversion arrives. They assume it will show up eventually,

and they design a process that quietly adapts. When stocks run hot, they trim back toward a target allocation.

When stocks fall, they addsometimes painfully, sometimes reluctantly, but consistently.

They rarely “nail” the top or bottom, yet over time they avoid extreme positioning.

Their advantage isn’t genius; it’s a system that reduces the odds of panic decisions.

The “Diversifier Who Avoids the One-Trade Trap”

In periods of narrow market leadership, this investor looks boring compared to friends who own only the hottest names.

Then leadership shifts, and suddenly boring looks brilliant.

Their experience of mean reversion is less about dramatic recovery and more about not being crushed by a single regime change.

They learn that diversification can feel like a drag… until it feels like a parachute.

The “Goal-First Investor”

This investor doesn’t ask, “When is mean reversion coming?” as much as they ask, “What would I do if it comes?”

They align their portfolio with time horizons: near-term money stays safer, long-term money stays invested,

and risk is sized to their real life, not their bravado.

When the market drops, they’re not thrilled, but they’re not forced to sell.

Their experience of mean reversion is still emotionalbecause they’re humanbut it’s not catastrophic.

They’ve built a structure that makes the market’s mood swings survivable.

The shared moral across these experiences is simple: mean reversion doesn’t just test your portfolioit tests your habits.

It punishes concentration, impatience, and identity-based investing (“I’m the person who always predicts the crash”).

And it rewards process: diversification, sensible rebalancing, and aligning risk with your actual life needs.

In other words, the best way to “beat” mean reversion is to stop treating it like an event to outsmart

and start treating it like weather you’re dressed for.