Table of Contents >> Show >> Hide

- What “Affordable Housing” Really Means

- The Era When a Home Felt Within Reach

- Why Housing Became So Expensive

- What Affordable Housing Looked Like in Daily Life

- The “Affordable” Past Was Not Perfect

- Where Housing Is Still More Affordable

- Why the Housing Crisis Feels Personal

- What Can Make Housing Affordable Again?

- Lessons From When Housing Was Affordable

- Experience Section: Remembering When Housing Felt Possible

- Conclusion

There was a time in America when buying a home did not require a spreadsheet, a second job, three roommates, a lucky inheritance, and the emotional stamina of a marathon runner. People still worried about money, of course. Nobody in 1978 was skipping into a bank with a lunchbox full of confidence and saying, “One house, please.” But for many middle-class families, housing once felt like a difficult goal rather than a fantasy novel.

Today, the phrase “when housing was affordable” sounds almost mythical, like “when airline seats had legroom” or “when concert tickets did not require a payment plan.” Home prices have risen faster than incomes in many markets, mortgage rates have climbed from pandemic-era lows, rents have eaten larger chunks of paychecks, and starter homes have become as rare as a polite comment section. The result is a housing affordability crisis that reaches renters, first-time buyers, growing families, retirees, and even homeowners who technically “won” the game but now face rising insurance, taxes, and repair costs.

So what happened? Why did housing affordability change so dramatically? And what can the era of affordable housing teach us about building a better market today? Let’s unpack the story without the usual economic fog machine.

What “Affordable Housing” Really Means

Housing is generally considered affordable when a household spends no more than 30% of its gross income on housing costs, including utilities. That benchmark is not perfect, but it is useful because it shows how much room a household has left for everything else: food, transportation, health care, savings, school expenses, birthday gifts, emergency car repairs, and the occasional pizza that prevents a family argument from becoming a documentary.

When a household spends more than 30% of income on housing, it is commonly called cost burdened. When it spends more than 50%, it is severely cost burdened. At that level, the budget is not tight; it is wearing a corset. Every unexpected expense becomes a crisis. A broken water heater, a medical bill, or a jump in rent can push a household into debt, relocation, or homelessness.

The Era When a Home Felt Within Reach

The golden age of housing affordability was not one single year. It varied by region, race, class, interest rate, and access to credit. Still, many Americans remember the decades after World War II through the late 20th century as a period when homeownership felt more attainable for a large share of working and middle-class families.

Several forces made that possible. The country built a lot of housing. Suburbs expanded. Land was cheaper in many metro areas. Wages for many workers rose alongside productivity. Mortgage products became more standardized. The 30-year fixed-rate mortgage gave buyers predictable payments. Government-backed lending helped expand access, although not equally or fairly for everyone. For many families, one steady income could cover a modest home, a used car, groceries, and maybe a vacation that involved a station wagon and a cooler full of sandwiches.

But the nostalgia needs an asterisk the size of a garage door. Housing was more affordable for many white families because discriminatory lending, redlining, exclusionary zoning, and unequal access to credit blocked many Black, Latino, Asian, and Indigenous households from the same opportunities. In other words, the old system was more affordable for some, but never fair for all.

Why Housing Became So Expensive

1. Home Prices Outran Incomes

The simplest explanation is also the most painful: homes got expensive faster than paychecks grew. A house is not just a product; it is land, labor, lumber, financing, regulations, location, school access, job access, and neighborhood demand bundled into one very expensive box with plumbing.

In many U.S. markets, the price-to-income ratio has stretched far beyond what previous generations faced. When prices rise faster than wages, buyers must borrow more, save longer, move farther out, buy smaller, or give up. That is why many younger adults are delaying homeownership, staying with family longer, renting longer, or moving to lower-cost regions.

2. Mortgage Rates Changed the Monthly Payment

Home prices get the headlines, but mortgage rates determine the monthly reality. A $400,000 home at 3% interest and a $400,000 home at 6% or 7% interest are not the same animal. One is a manageable house payment for some households; the other may look like it swallowed the grocery budget.

During the pandemic, extremely low mortgage rates helped buyers stretch. But when rates rose sharply, the same home suddenly required a much higher income. This created a strange market: many existing homeowners stayed put because they did not want to trade a low-rate mortgage for a higher-rate one. That “lock-in effect” reduced the number of homes for sale, which kept supply tight and prices stubborn.

3. America Did Not Build Enough Homes

For years, the United States underbuilt housing relative to demand. After the 2008 housing crash, construction slowed. Builders became cautious. Labor shortages, higher materials costs, local opposition, zoning limits, and complicated permitting made new construction harder and more expensive.

The shortage is especially severe in job-rich metro areas where people want to live. When a city adds jobs but not enough homes, prices rise. It is not magic; it is musical chairs with mortgages. If 100 families want homes and only 70 homes are available, the highest bidders win and everyone else gets pushed outward.

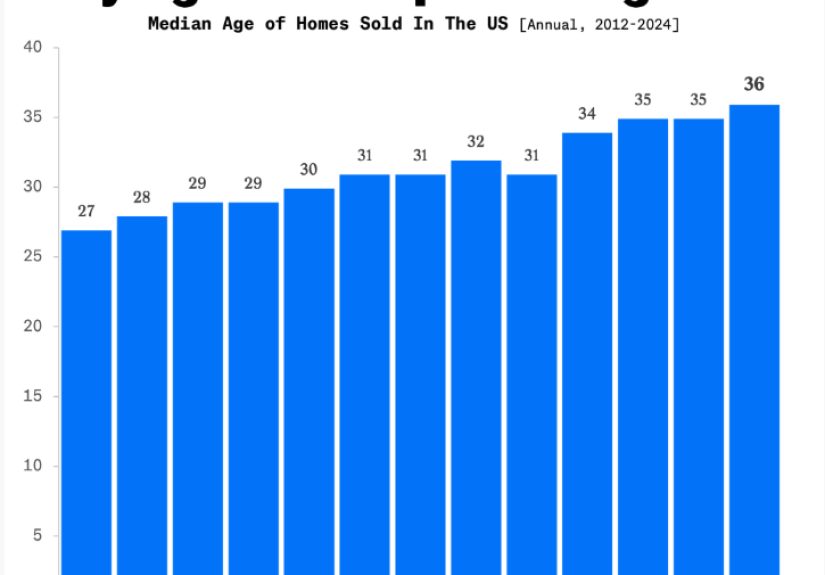

4. Starter Homes Nearly Disappeared

Affordable starter homes used to be the first rung on the homeownership ladder. They were small, simple, and sometimes decorated with wallpaper that could emotionally damage a visitor. But they gave first-time buyers a way in.

Today, many builders focus on larger homes because land, labor, financing, and regulatory costs make smaller homes less profitable. In many communities, zoning rules also limit duplexes, triplexes, cottage courts, manufactured homes, accessory dwelling units, and small-lot homes. The result is a market that produces plenty of “dream homes” and not enough “please just let me build equity before I turn 50” homes.

5. Renters Got Squeezed Too

When buying becomes harder, more people remain renters. When more people rent and rental supply is limited, rents rise. That is why the housing affordability crisis is not only a buyer problem. It is also a renter problem, a student problem, a senior problem, and a workforce problem.

In many cities, renters are spending well above the 30% affordability threshold. For lower-income renters, the situation is especially severe. A household earning $30,000 per year cannot simply “budget better” its way out of a $1,700 monthly rent. At some point, math stops being motivational and starts being a brick wall.

What Affordable Housing Looked Like in Daily Life

When housing was more affordable, families had more breathing room. A monthly payment did not consume the entire paycheck. People could save for repairs, education, retirement, and emergencies. A teacher, postal worker, nurse, mechanic, or factory employee could often live reasonably near work. Young adults could move out earlier. Families could grow without treating every extra bedroom like a luxury upgrade.

Affordable housing also shaped communities. Schools had more stable enrollment. Local businesses could hire workers who lived nearby. Grandparents could remain close to grandchildren. People had enough financial slack to volunteer, start small businesses, or survive a temporary setback.

That is what gets lost when housing becomes unaffordable. The issue is not just whether someone can buy a house. It is whether a community can function when the people who teach, cook, repair, drive, care, clean, and serve cannot afford to live there.

The “Affordable” Past Was Not Perfect

It is tempting to imagine the past as a sepia-toned paradise where everyone bought a bungalow at age 24 and paid it off using pocket change and gumption. Reality was messier. Mortgage rates were extremely high in parts of the late 1970s and early 1980s. Many homes lacked modern energy efficiency. Some neighborhoods excluded people through law, lending, or intimidation. Women often faced credit discrimination. Minority households were denied wealth-building opportunities that helped other families climb the property ladder.

So the goal should not be to recreate the past. The goal should be to recover what workedreasonable price-to-income ratios, abundant starter homes, stable financing, and real pathways into ownershipwhile rejecting the discrimination and exclusion that shaped too much of the old system.

Where Housing Is Still More Affordable

Housing affordability has not disappeared everywhere. Some Midwestern and Southern markets still offer lower price-to-income ratios than coastal metros. Cities such as Pittsburgh, Cleveland, St. Louis, Oklahoma City, and parts of Texas, Ohio, Indiana, and Pennsylvania have often remained more attainable than places like San Jose, Los Angeles, New York, Seattle, Boston, and San Diego.

But even in lower-cost markets, affordability can be fragile. If wages are low, a cheaper house may still be difficult to buy. If insurance premiums rise, property taxes jump, or investors buy up entry-level homes, the advantage can shrink quickly. Affordable does not simply mean “less expensive than California.” It means local households can realistically afford local housing.

Why the Housing Crisis Feels Personal

Housing is emotional because it is not just an investment. It is where people sleep, argue, cook, raise children, recover from illness, decorate badly, host holidays, and store mystery cables in a drawer forever. When housing is unstable, everything else becomes unstable.

For younger buyers, the frustration is sharp. Many did what they were told: studied, worked, saved, avoided unnecessary debt, and tried to be responsible. Then they entered a market where the down payment kept moving like a finish line on roller skates.

For renters, the pain is monthly. Rent increases can erase raises. Application fees, deposits, pet rent, parking fees, and moving costs add up. Even people with decent incomes may feel stuck because saving for a down payment while paying high rent is like trying to fill a bathtub with the drain open.

For older homeowners, affordability has a different face. Some own their homes but struggle with taxes, insurance, utilities, maintenance, and accessibility upgrades. A paid-off home does not feel paid off when the roof needs replacing and the insurance bill arrives wearing tap shoes.

What Can Make Housing Affordable Again?

Build More Homes in More Shapes

Supply matters. America needs more homes, especially homes that ordinary households can afford. That means not only single-family houses, but also duplexes, townhomes, apartments, accessory dwelling units, manufactured homes, senior housing, and small starter homes.

Communities that allow more flexible housing types can create more options at different price points. Not every household needs a four-bedroom house on a large lot. Some people need a small condo near transit. Others need a backyard cottage for an aging parent. Others need a modest starter home that does not come with a luxury kitchen island the size of a canoe.

Fix Zoning and Permitting Bottlenecks

Local rules can make housing more expensive by limiting where and what builders can construct. Minimum lot sizes, parking requirements, height limits, and lengthy approval processes can raise costs before a shovel touches dirt.

Reform does not mean building chaos. It means allowing enough housing in enough places so that demand does not crush supply. Good planning can add homes while protecting safety, infrastructure, trees, schools, and neighborhood character. The key is to stop treating every new home as an invading spaceship.

Support First-Time Buyers

Down payment assistance, lower-cost financing, shared equity models, and targeted support for first-generation buyers can help households that have income but lack family wealth. This matters because many buyers today are competing against people who receive parental help, investment gains, or equity from a previous home.

However, buyer assistance works best when paired with more supply. If governments help buyers but do not add homes, extra purchasing power can simply bid up prices. That is like handing everyone a bigger bucket while refusing to fix the water shortage.

Preserve Affordable Rentals

Building new homes is essential, but preserving existing affordable rentals is just as important. Older apartment buildings, small multifamily properties, manufactured home communities, and naturally affordable housing often provide lower-cost options without needing a new ribbon-cutting ceremony.

Preservation can include repair funds, nonprofit acquisition, tax incentives, tenant protections, and financing tools that keep affordable units from disappearing. Once affordable housing is lost, replacing it is usually more expensive.

Make Housing Costs More Predictable

Insurance, taxes, utilities, and maintenance are now major affordability issues. A homebuyer who can afford the mortgage may still struggle if insurance premiums jump or property taxes rise quickly. Policymakers, lenders, and consumers need to look at total housing cost, not just the sale price.

Energy efficiency upgrades, resilient construction, fair insurance markets, and property tax relief for vulnerable homeowners can help stabilize costs. Affordability is not only about getting into a home; it is about staying there.

Lessons From When Housing Was Affordable

The main lesson is not that the past was perfect. It is that housing affordability is built by choices. The United States once built more modest homes, financed them with predictable loans, and allowed more households to turn income into ownership. At the same time, the country also excluded millions from those benefits. A better future must be both more affordable and more inclusive.

Another lesson is that housing markets are local, but the consequences are national. When housing costs rise, workers cannot move to opportunity. Families delay milestones. Businesses struggle to hire. Children experience school instability. Seniors face isolation. Homelessness rises. Household debt grows. The economy becomes less flexible and less fair.

Finally, affordable housing is not a luxury policy topic for urban planners and people who enjoy zoning meetings, though bless them for their endurance. It is a kitchen-table issue. It determines whether people can start families, change jobs, save money, care for relatives, and build wealth.

Experience Section: Remembering When Housing Felt Possible

Talk to people who bought homes decades ago, and the stories often sound unbelievable to younger listeners. Someone’s parents bought a small ranch house on one income. A teacher and a mechanic purchased a starter home after saving for a few years. A newly married couple moved into a fixer-upper and slowly improved it room by room. The house was not glamorous. The carpet may have been a color best described as “1970s soup.” The kitchen may have had cabinets that squeaked like haunted furniture. But the numbers worked.

That is the part people miss most: not perfection, but possibility. The affordable house of memory was often modest. It had one bathroom, not a spa retreat. The basement was unfinished. The driveway cracked. The yard needed work. Nobody expected quartz countertops, smart appliances, and a walk-in closet with its own emotional support lighting. Buyers accepted imperfections because the home was a beginning, not a final boss battle.

In many families, the first home became a classroom. People learned how to paint walls, replace faucets, patch drywall, plant shrubs, argue about thermostat settings, and discover that “quick weekend project” is one of the funniest phrases in the English language. Homeownership created forced savings, but it also created practical confidence. Every repair made the place feel more personal. Every mortgage payment built a little more equity. Every holiday made the house more than an asset.

For renters, affordability once meant mobility. A young adult could rent an apartment, pay bills, and still save something. A family could move for a better job without losing half its income to rent. A senior could downsize without entering a luxury-priced rental market. Affordable rent gave people options, and options are a quiet form of freedom.

The modern experience is different. Many renters feel like they are running on a treadmill that charges application fees. Many buyers tour homes with old roofs, tiny kitchens, and bidding wars anyway. Parents worry their children will not live near them. Workers commute farther because they cannot afford the communities they serve. People who earn respectable salaries still feel behind because housing has become the biggest gatekeeper in American life.

Yet the memory of affordability is useful because it proves the current crisis is not inevitable. Housing did not become expensive by gravity. It became expensive through shortages, rules, financing conditions, land costs, wage gaps, speculation, and years of delayed decisions. That also means affordability can improve through better decisions: more homes, more starter options, smarter zoning, fairer lending, stronger rental supply, and policies that treat housing as essential infrastructure rather than a luxury collectible.

When housing was affordable, people did not feel rich. They felt stable. They felt that effort could lead somewhere. They felt the future had a front door. That is the feeling worth rebuilding.

Conclusion

“When housing was affordable” is more than a nostalgic phrase. It is a reminder that a healthy housing market should allow working people to rent safely, buy realistically, move when opportunity calls, and stay rooted when life gets hard. The United States cannot solve affordability with one magic policy, one interest-rate cut, or one motivational speech about skipping lattes. It needs more supply, better land-use rules, preserved rentals, support for first-time buyers, and a renewed commitment to making housing a foundation for stability.

The past offers both inspiration and warning. Affordable housing helped many families build security, but unequal access kept others out. The next era of affordability must do better: more homes, more choices, more fairness, and fewer households forced to choose between a roof and the rest of life.

![18 Best Types of Charts and Graphs for Data Visualization [+ How to Choose]](https://corkopencoffee.org/wp-content/uploads/2026/05/18-best-types-of-charts-and-graphs-for-data-visualization-how-to-choose-qKM1PBYG-thumb.jpg)