Table of Contents >> Show >> Hide

- What Makes an Investment Track Record “Impressive” (Not Just “Lucky”)?

- The Contenders: Legends, Records, and the Fine Print

- So… Who Wins? It Depends on Your Scorecard

- What This Means for Normal Investors: Build Your Own “Impressive Track Record”

- The Great Irony: Even When Skill Exists, Investors Often Don’t Capture It

- Conclusion: The Best Track Record Is the One That Survives Reality

- Experiences That Match the Question: “Who Has the Most Impressive Track Record?”

Who’s the greatest investor of all time? It’s the finance-world version of “Jordan or LeBron?”except instead of highlights, we argue with spreadsheets and then pretend we enjoyed it.

Ben Carlson at A Wealth of Common Sense tackled this exact debate, and it’s a fun one because it forces a question most investors dodge: what do we even mean by “best track record”? Raw returns? Risk-adjusted results? Longevity? Doing it at massive scale? Or doing it in a way that normal humans can actually copy without needing a PhD, a supercomputer, or a time machine?

Let’s define “impressive” in a way that doesn’t fall apart the moment you poke it with a diversification stickthen run the usual legends through the test. Spoiler: the answer depends on what you value. But also… it’s probably Buffett. (Try saying that out loud in a room full of hedge fund managers. It’s like yelling “free refills” in a fancy restaurant.)

What Makes an Investment Track Record “Impressive” (Not Just “Lucky”)?

It’s easy to crown a champion if your entire scoring system is “who had the biggest number on the screen for a few years.” The problem: markets are noisy, styles rotate, and luck can dress up as genius for longer than you’d think.

1) Time: Can You Do It Across Multiple Market Regimes?

One bull market can make almost anyone look like a wizard. A truly elite record survives:

- High inflation and low inflation

- Recessions and expansions

- Rising rates and falling rates

- Tech booms, value revivals, and the occasional “what even is happening?” year

2) Scale: How Hard Is It to Repeat With Real Money?

Turning $10,000 into $100,000 is impressive. Turning $10 billion into $100 billion while the whole world watches? That’s a different sport. Scale creates friction: fewer opportunities, higher trading costs, more competition, and a very real “your own success limits your future success” problem.

3) Transparency: Can We See the Process, or Just the Outcome?

A record that’s independently observablepublic filings, audited results, long-running shareholder letterscounts differently than performance that’s mostly whispered about in reverent tones over expensive coffee.

4) Risk: How Much Volatility, Leverage, and Drawdown Came With It?

Return without context is like reading a restaurant review that only says, “The portions were huge.” Great! Were they… good? Risk-adjusted measures (like Sharpe ratio) try to capture how much return you earned per unit of volatility. They’re imperfect, but they’re better than judging investors by the financial equivalent of a single Instagram photo.

5) Accessibility: Could a Non-Insider Actually Benefit From It?

If the “best track record ever” happened in a fund closed to outsiders, it’s still fascinatingbut it’s less useful for most investors. It’s like naming the best pizza in America… and then learning it’s only served on a submarine.

The Contenders: Legends, Records, and the Fine Print

Here are a few names that constantly show up in “greatest investor” debateseach impressive, each complicated.

Jim Simons: The Track Record That Looks Like a Typo

Jim Simons and Renaissance Technologies are the stuff of Wall Street mythology: quantitative models, brilliant scientists, relentless data, and returns that (allegedly) make your calculator ask for a break.

Simons’ Medallion Fund is frequently cited as one of the greatest performances in investing history. The catch is that it’s not meaningfully investable for the public and has hard capacity limits. In other words, even if you fully believe the results, you can’t just “buy Simons” in your retirement account the way you can buy an index fund.

Why it’s impressive: extreme compounding over decades, systematic edge, and a willingness to close to new capital when scale threatened the strategy.

Why it’s tricky: secrecy, limited accessibility, and the uncomfortable reality that “incredible” does not automatically mean “repeatable for everyone at any size.”

Peter Lynch: The Most Famous Mutual Fund Run in History

Peter Lynch is the patron saint of “regular people can do this.” While managing Fidelity’s Magellan Fund, he became known for plain-English investing principles and a willingness to hunt across the marketincluding smaller companies most giant institutions couldn’t touch back then.

Why it’s impressive: standout performance over a long stretch, in a public mutual fund, with a philosophy many investors can understand.

Why it’s tricky: Magellan’s environment was uniquemore market inefficiencies, fewer quant competitors, and a world where “information” didn’t travel at the speed of a notification.

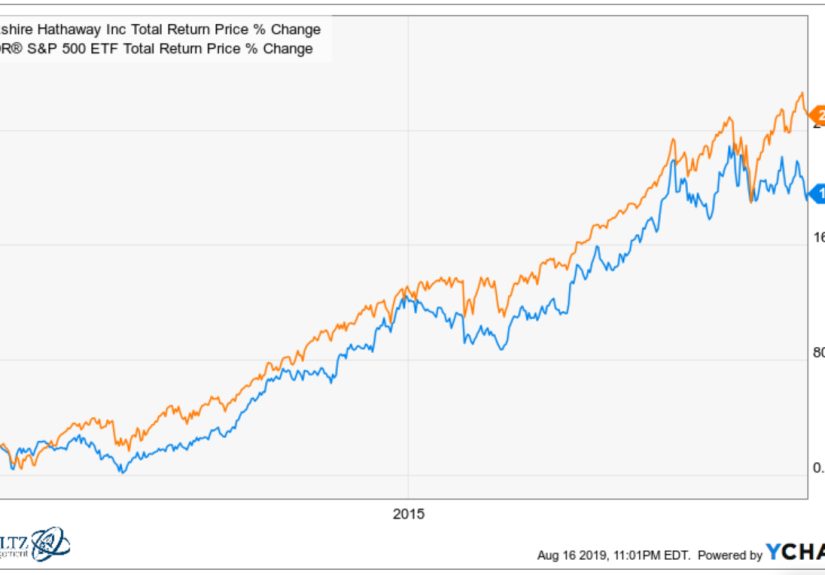

Warren Buffett: The Compounding Machine With a Shareholder Letter

Buffett’s record sits in a rare sweet spot:

- Long duration: measured in decades, not quarters

- Massive scale: not a niche strategy that breaks when it gets popular

- Public accountability: shareholders, reporting, and a paper trail

- Business building: he didn’t just pick stockshe built a capital allocation engine

Buffett’s approach also illustrates something many “great investor” lists miss: sometimes the edge is structure, not just stock selection. Berkshire’s permanent capital and insurance operations created a durable advantageone that’s difficult for typical fund managers to replicate under quarterly performance pressure.

David Swensen: Institutional Greatness (and the Replication Trap)

Swensen’s work at the Yale endowment helped popularize the “endowment model,” emphasizing diversification beyond public stocks and bondsespecially into private markets and other alternatives.

Why it’s impressive: long-term institutional compounding and thoughtful portfolio construction.

Why it’s tricky: many investors tried to copy the Yale model without Yale’s access, manager selection capability, fees, liquidity tolerance, and governance. Replication often turns into “the expensive version of diversification.”

Sir John Templeton: Global Value Before It Was Cool

Templeton’s reputation comes from global, contrarian value investingleaning into “maximum pessimism” when others were sprinting away from it. His legacy is as much about temperament and long-term thinking as it is about specific trades.

So… Who Wins? It Depends on Your Scorecard

If your only metric is “highest reported returns,” you’ll be tempted to crown strategies like Medallion. If your metric is “most educational for average investors,” you might lean toward Lynch. If your metric is “best institutional allocator,” Swensen enters the chat.

But if you combine the big criterialongevity + scale + transparency + adaptabilityBuffett is the most defensible answer, and that’s essentially where A Wealth of Common Sense lands.

Why Buffett’s Track Record Is a Category of Its Own

- He did it for an absurdly long time. Many investors have hot streaks. Very few have multi-decade dominance.

- He did it at enormous scale. As Berkshire grew, the game got harderyet the machine kept compounding.

- He made it observable. Shareholder letters, public reporting, and a consistent philosophy across cycles.

- He played the real-world game. Taxes, turnover, incentives, capital structure, and human psychologyBuffett’s edge wasn’t just “good picks,” it was building a system that made good decisions easier to repeat.

What This Means for Normal Investors: Build Your Own “Impressive Track Record”

Here’s the slightly annoying truth: most investors don’t need to find the world’s greatest investor. They need to stop sabotaging themselves with:

- Performance chasing

- Overtrading

- Overconfidence in forecasts

- Underestimating fees and taxes

- Panic-selling when the headlines get spicy

The most impressive track record you can realistically pursue is your own: a repeatable process that compounds steadily and survives the moments when your emotions try to stage a coup.

A Practical “Track Record Checklist” (For Funds, Managers, or Your Own Plan)

- Benchmark clarity: What are we comparing against, and is it fair?

- Time horizon: Is the record long enough to include ugly markets?

- Risk profile: What were the worst drawdowns and how quickly did it recover?

- Fees & taxes: Is the “edge” mostly getting eaten by costs?

- Consistency of process: Can they explain what they do without relying on magic words?

- Capacity constraints: Can this strategy work at today’s asset level?

The Great Irony: Even When Skill Exists, Investors Often Don’t Capture It

One reason “great track records” don’t translate into great investor outcomes is behavior. Many investors buy after a run of outperformance and sell after a slumpturning compounding into a game of “buy high, sell low,” which is a surprisingly popular hobby for people who claim to hate losing money.

That’s why the best long-term strategy for most people looks boring: low-cost diversification, an asset allocation you can stick with, and a written plan for what you’ll do when the market inevitably tries to scare you out of it.

Conclusion: The Best Track Record Is the One That Survives Reality

Jim Simons may have the most jaw-dropping numbers. Peter Lynch may be the most relatable stock-picking legend. Swensen may be the allocator’s allocator. Templeton may be the most temperamentally inspiring.

But when you combine longevity, scale, transparency, and a repeatable philosophy, Buffett stands out as the most impressive all-around investment track recordexactly the kind of “greatness” that holds up even when you stop cheering and start measuring.

Experiences That Match the Question: “Who Has the Most Impressive Track Record?”

(These are common real-world investor experiences and patternswhat people tend to live through when they chase greatness, try to copy it, or decide to build it slowly.)

Experience #1: The “Hot Hand” Trap (a.k.a. Buying the Trophy After the Parade)

You notice a fund (or strategy) that just crushed it. The chart is gorgeous. The headlines are glowing. Your brain begins negotiating: “This isn’t chasing performance, it’s recognizing excellence.” So you buyright when expectations are highest and the strategy is most crowded.

Then comes the perfectly normal part of investing: a slump. Not a scandal. Not a fraud. Just a stretch where the strategy underperforms. Suddenly the same record that made you feel safe now feels like evidence you were fooled. You sell, promising yourself you’ll “get back in later.” Later usually means higher pricesbecause discipline is hard, and regret is louder than logic.

The lesson most investors learn the hard way: a great historical track record doesn’t protect you from future discomfort. If you don’t have a plan for the ugly stretches, you won’t capture the beautiful long-term average.

Experience #2: The Buffett Cosplay (Buying “Quality” Without Buying Patience)

A lot of investors try to “invest like Buffett” by purchasing a handful of well-known, high-quality companies and then watching them… hourly. Which is kind of like trying to “live like a monk” by buying a meditation cushion and then hosting loud parties on it.

The real Buffett experience isn’t just buying great businessesit’s sitting still while everyone else is losing their mind. Most people underestimate how psychologically expensive patience can be. When a stock drops 30%, your brain doesn’t say, “Wonderful, a better expected return!” It says, “Congratulations, you have invented a new form of embarrassment.”

The investors who actually get something Buffett-like out of the market aren’t the ones who copy his holdings. They copy his time horizon, his focus on fundamentals, and his willingness to look wrong for long stretches before being right.

Experience #3: The Quiet Track Record (Compounding Without Needing a Hero)

Some investors eventually stop hunting for the single greatest investor and start building a system: automatic contributions, diversified funds, periodic rebalancing, and a “do nothing dramatic” policy when volatility hits.

At first it feels underwhelming. There’s no thrilling story to tell at dinner. Nobody gasps when you say, “I contributed monthly and rebalanced once a year.” (If they do, marry them.) But over time, this approach creates a personal track record that is both impressive and attainable: steady compounding, fewer mistakes, and a plan that survives real life.

The big realization: the most valuable edge most investors can get isn’t secret researchit’s behavioral consistency. The boring approach wins because it’s the one you can keep doing.